Execution Guides for Indian Investors

Learning about investing is important. But eventually, every investor reaches the same point where knowledge must turn into action.

You may understand stocks, mutual funds, ETFs, bonds, and SIPs. Yet when it comes time to actually place an order, start a SIP, buy an ETF, or invest in a bond, uncertainty often appears. Questions such as “Which option should I select?”, “What happens after I click Buy?”, or “Am I doing this correctly?” are more common than most beginners realize.

The purpose of this section is not to tell you what to buy. Instead, it is designed to help you understand how investing works in practice. From buying stocks and ETFs to starting SIPs, investing in bonds, and understanding order types, these lessons focus on the execution side of investing—the part where theory becomes action.

No stock tips. No predictions. No shortcuts.

Just practical guidance to help you invest with greater confidence, avoid common mistakes, and understand what happens before, during, and after every investment decision.

Lesson 1: Investing Execution – From Theory to Action

Why This Lesson Matters

Most beginners make the same mistake.

They start by asking:

- Which stock should I buy?

- Which mutual fund is best?

- Which ETF should I choose?

- Where should I invest first?

These questions seem logical.

But they skip an important step.

Before deciding what to buy, you should first understand the different investment options available and how they fit into your financial journey.

Imagine entering a large shopping mall without knowing what you need.

You may buy something.

But you probably won’t make the best decision.

Investing works the same way.

The purpose of this lesson is to give you a clear map of the investment landscape before we begin learning how to execute different types of investments.

The Five Major Investment Routes

Most retail investors in India eventually invest through one or more of these routes:

INVESTING

│

┌──────────┬────────┼────────┬──────────┐

│ │ │ │ │

Stocks ETFs Mutual Bonds SIP

Funds

At first glance, these may appear similar.

They are not.

Each serves a different purpose.

Understanding these differences will help you make better decisions later.

Route 1: Stocks (Direct Equity Investing)

What Are Stocks?

When you buy a stock, you become a partial owner of a business.

If you purchase shares of:

- Reliance Industries

- Infosys

- TCS

- HDFC Bank

you become a shareholder of that company.

You are no longer just a customer.

You become an owner.

Your investment performance is linked to the success or failure of the business.

Where Do You Buy Stocks?

Stocks are purchased through:

✔ Broker

✔ Trading Account

✔ Demat Account

✔ Stock Exchange (NSE/BSE)

The process looks like this:

Bank Account

↓

Trading Account

↓

NSE / BSE

↓

Demat Account

Example

Suppose you buy one share of Infosys.

After the order executes:

- Money leaves your bank account.

- Shares are credited to your Demat account.

- You become a shareholder.

Simple.

Who Should Consider Stocks?

Stocks may suit investors who:

- Enjoy research

- Want direct ownership

- Can tolerate volatility

- Have a long-term mindset

What Most Beginners Don’t Realize

Buying stocks is easy.

Choosing the right stocks is difficult.

Many investors underestimate this difference.

Route 2: ETFs (Exchange Traded Funds)

What Is an ETF?

ETF stands for:

Exchange Traded Fund

An ETF is a basket of investments that trades on the stock exchange like a stock.

Think of it as buying many investments through a single transaction.

Example

Suppose you buy a Nifty 50 ETF.

Instead of purchasing:

- Reliance

- Infosys

- HDFC Bank

- ICICI Bank

- TCS

individually,

you gain exposure to all of them through one purchase.

Where Do You Buy ETFs?

This is extremely important.

Many beginners assume ETFs work like mutual funds.

They don’t.

ETFs are purchased exactly like stocks.

You need:

✔ Broker

✔ Trading Account

✔ Demat Account

✔ Stock Exchange

Example

Buying a Nifty ETF looks almost identical to buying Infosys shares.

The difference is what you own.

One gives exposure to a company.

The other gives exposure to a basket of investments.

Who Should Consider ETFs?

ETFs may suit investors who:

- Want diversification

- Prefer simplicity

- Like passive investing

- Want lower costs

What Most Beginners Don’t Realize

Many investors spend months trying to identify the perfect stock.

An ETF allows them to participate in a broader market opportunity with a single investment.

Route 3: Mutual Funds

What Is a Mutual Fund?

A mutual fund pools money from thousands of investors.

A professional fund manager then invests that money according to the fund’s objective.

Instead of making every investment decision yourself, you delegate that responsibility.

Example

Imagine investing in 40 companies.

You could:

Option A

Research all 40 companies yourself.

or

Option B

Allow a professional fund manager to manage the portfolio.

Mutual funds provide Option B.

Where Do You Buy Mutual Funds?

Unlike ETFs, mutual funds are usually purchased through:

- AMC Websites

- Mutual Fund Platforms

- Broker Apps

- Investment Platforms

In most cases:

You do not need a Demat account.

This is one of the biggest differences between ETFs and mutual funds.

Who Should Consider Mutual Funds?

Investors who:

- Have limited time

- Prefer professional management

- Want diversification

- Do not enjoy stock research

What Most Beginners Don’t Realize

The best mutual fund is not necessarily the fund with the highest recent return.

The best mutual fund is often the one that aligns with your goals and allows you to remain invested for years.

Route 4: SIP (Systematic Investment Plan)

What Is a SIP?

This is one of the most misunderstood concepts in investing.

Many people believe:

SIP is an investment.

This is incorrect.

A SIP is simply a method of investing.

Think About It Like This

Mutual Fund = Destination

SIP = Journey Method

The mutual fund is the investment.

The SIP is the process used to invest regularly.

Example

Suppose you invest:

₹5,000 every month

into a mutual fund.

The mutual fund is the investment.

The SIP is merely the mechanism used to make recurring investments.

When Does SIP Make Sense?

SIPs are often useful when:

- You earn a monthly salary.

- You want investing discipline.

- You prefer gradual investing.

- You don’t want to worry about timing the market.

What Most Beginners Don’t Realize

A SIP does not guarantee profits.

A SIP simply creates consistency.

The quality of the investment still matters.

SIP vs Lump Sum

This deserves special attention.

SIP Example

You earn ₹80,000 per month.

You decide to invest ₹10,000 monthly.

A SIP naturally fits your cash flow.

Lump Sum Example

You receive:

- Annual Bonus

- Inheritance

- Property Sale Proceeds

You already have the money available.

A lump sum investment becomes possible.

Which Is Better?

There is no universal answer.

The decision depends on:

- Cash flow

- Market conditions

- Risk tolerance

- Personal preference

Route 5: Bonds & Debt Instruments

What Is a Bond?

When you buy a bond, you are lending money.

The issuer agrees to:

- Pay interest

- Return principal at maturity

Example

Suppose a company issues a bond.

Instead of becoming an owner (as with stocks),

you become a lender.

Who Issues Bonds?

- Government

- Public Sector Companies

- Private Companies

Where Can You Buy Bonds?

Depending on the product:

- Stock Exchanges

- Bond Platforms

- Banks

- RBI Retail Direct

- Primary Bond Issues

Who Should Consider Bonds?

Investors seeking:

- Stability

- Income generation

- Lower volatility

What Most Beginners Don’t Realize

The purpose of bonds is not maximizing returns.

The purpose of bonds is balancing risk and providing stability.

A Simple Decision Framework

Before choosing an investment route, ask yourself:

Do I enjoy researching businesses?

YES

→ Stocks

NO

→ ETFs or Mutual Funds

Do I want professional management?

YES

→ Mutual Funds

NO

→ ETFs

Do I want to invest every month automatically?

→ SIP

Do I need stability and regular income?

→ Bonds

Why Execution Matters

Now that you understand the major investment routes, the next challenge is execution.

Knowing:

- What a stock is

- What an ETF is

- What a mutual fund is

does not automatically tell you:

- How to buy it

- Which order type to use

- What happens after purchase

- What mistakes to avoid

This is where execution becomes important.

Every investment decision eventually reaches the same moment:

The Buy button.

The lessons that follow will focus on helping you navigate that moment with confidence.

Key Takeaway

Before learning how to invest, understand what you can invest in.

Stocks, ETFs, mutual funds, SIPs, and bonds all serve different purposes.

The best choice depends on:

- Your goals

- Your knowledge

- Your available time

- Your risk tolerance

- Your investing style

There is no single “best” investment for everyone.

Successful investors choose the right tool for the right purpose.

In the next lesson, we will begin with stocks and ETFs and learn exactly how they are bought, how order types work, and what mistakes beginners should avoid when placing their first investment order.

Lesson 2: How to Buy Stocks & ETFs Correctly

Understanding Ownership, Diversification, and the Mechanics of Your First Purchase

Why This Lesson Matters

For many investors, the first real investing decision is not:

“Which stock should I buy?”

The first real decision is:

“Should I buy individual stocks at all?”

This question is often overlooked.

Yet it can have a significant impact on an investor’s journey.

Some investors enjoy researching businesses and building concentrated portfolios.

Others prefer broad diversification through ETFs.

Neither approach is automatically right or wrong.

The better choice depends on:

- Your knowledge

- Available time

- Interest in research

- Risk tolerance

- Investing goals

Before placing your first order, it is important to understand what you are buying and why.

Part 1: Understanding Stocks

What Are You Actually Buying?

When you purchase a stock, you become a part-owner of a business.

This sounds simple.

But it changes how you should think about investing.

Many beginners see a stock as:

- A price chart

- A ticker symbol

- A trading opportunity

Experienced investors see something different.

They see a business.

Example

Imagine a local restaurant generates:

- Strong profits

- Loyal customers

- Consistent growth

If you could own a small piece of that business, you might be interested.

Publicly listed companies operate on the same principle.

The difference is that ownership is divided into shares.

When you buy shares, you become one of the owners.

What Determines Your Returns?

Over the long term, stock returns are generally influenced by:

- Revenue growth

- Profit growth

- Competitive strength

- Management quality

- Capital allocation

Short-term price movements may be unpredictable.

Long-term business performance matters much more.

Why Investors Like Stocks

Potential for Wealth Creation

Many of the world’s greatest wealth-building stories have come from business ownership.

Direct Control

You decide:

- Which company to own

- How much to invest

- When to buy

- When to sell

Opportunity to Outperform

If your research is strong, individual stocks may outperform the broader market.

The Challenge With Stocks

There is a trade-off.

Greater opportunity often comes with greater responsibility.

Example

Suppose you invest your entire portfolio into one company.

If the business succeeds:

Excellent outcome.

If the business struggles:

Your portfolio may suffer significantly.

This is known as concentration risk.

Many beginners underestimate it.

Part 2: Understanding ETFs

What Is an ETF?

ETF stands for:

Exchange Traded Fund

Think of an ETF as a basket of investments packaged into a single security.

Instead of buying one company, you buy exposure to many companies through one transaction.

Example

Imagine you want exposure to India’s largest companies.

Option 1:

Purchase 50 individual stocks separately.

Option 2:

Purchase a Nifty 50 ETF.

One transaction.

Broad diversification.

Same objective.

This is why ETFs have become popular around the world.

What Determines ETF Performance?

The answer depends on what the ETF tracks.

Examples:

Nifty ETF

Tracks the Nifty 50 Index.

Sensex ETF

Tracks the Sensex.

Gold ETF

Tracks gold prices.

International ETF

Tracks foreign markets.

The ETF’s performance generally reflects the underlying assets it owns.

Why Investors Like ETFs

Instant Diversification

One purchase can provide exposure to dozens or even hundreds of securities.

Simplicity

No need to analyze individual businesses.

Lower Decision Burden

Investors spend less time worrying about:

- Which company to buy

- When to switch stocks

- Which management team is better

Lower Costs

Many ETFs are relatively inexpensive compared to actively managed funds.

The Challenge With ETFs

The primary trade-off is straightforward.

You gain diversification.

But you give up the possibility of dramatically outperforming the market through superior stock selection.

An ETF generally aims to match a market.

Not beat it.

Stocks vs ETFs: Which Should You Choose?

Many beginners believe they must choose one or the other.

This is not always true.

Some investors use both.

However, understanding the strengths of each approach is important.

| Stocks | ETFs |

|---|---|

| Ownership of individual companies | Ownership of a basket of investments |

| Requires research | Requires less research |

| Higher potential reward | Broad market exposure |

| Higher concentration risk | Lower concentration risk |

| Greater decision-making responsibility | Simpler management |

A Practical Framework

Choose Stocks If:

✔ You enjoy business analysis.

✔ You are willing to learn.

✔ You can tolerate volatility.

✔ You want direct ownership.

Choose ETFs If:

✔ You prefer simplicity.

✔ You want diversification.

✔ You have limited time.

✔ You believe broad market participation is sufficient.

Where Do You Buy Stocks & ETFs?

One of the most important things beginners should understand:

Stocks and ETFs are purchased exactly the same way.

You need:

✔ Broker

✔ Trading Account

✔ Demat Account

✔ Linked Bank Account

Purchase Flow

Bank Account

↓

Trading Account

↓

NSE / BSE

↓

Demat Account

After purchase:

Money leaves your bank account.

Ownership appears in your Demat account.

Understanding Order Types

Now we arrive at one of the most important execution decisions.

When placing an order, investors usually encounter:

Market Order

Limit Order

Understanding the difference can prevent unnecessary mistakes.

Market Orders

A market order executes immediately at the best available price.

Example

Current Price:

₹1,000

You place a market order.

The order executes instantly.

However, if prices move rapidly, execution may occur at:

₹1,002

₹1,005

or even higher.

You receive speed.

But less price control.

Best For

Highly liquid securities where immediate execution matters.

Limit Orders

A limit order allows you to define the maximum price you are willing to pay.

Example

Current Price:

₹1,000

You place a limit order at:

₹995

If the price reaches ₹995:

Order executes.

If it doesn’t:

Order remains pending.

You receive greater control.

But execution is not guaranteed.

Best For

Investors who prioritize price discipline over immediate execution.

Delivery vs Intraday

This is one of the most important distinctions beginners must understand.

Delivery (CNC)

Shares are credited to your Demat account.

You continue owning them after market hours.

This is generally the appropriate choice for long-term investing.

Intraday (MIS)

Position is intended to be opened and closed within the same trading day.

Often involves higher risk and additional complexity.

Important Rule For Beginners

If your objective is investing rather than trading:

Delivery is usually the correct choice.

Many beginners accidentally choose intraday without understanding the consequences.

Avoid that mistake.

Common Beginner Mistakes

Buying Without Understanding the Business

Price movement is not research.

Concentrating Too Much Money in One Stock

Diversification exists for a reason.

Chasing Trending Stocks

Popularity is not a substitute for analysis.

Using Order Types Blindly

Always understand what you are selecting.

Confusing Investing With Trading

The two activities require different skills and mindsets.

Before You Click Buy

Ask yourself:

What am I buying?

Why am I buying it?

Do I understand the business or ETF?

Am I investing or trading?

Am I comfortable holding this investment during market volatility?

If you can answer these questions confidently, execution becomes much easier.

Key Takeaway

Stocks and ETFs are purchased through the same infrastructure but serve different purposes.

Stocks provide direct ownership and greater upside potential, while ETFs offer diversification and simplicity.

Neither is automatically superior.

The right choice depends on your goals, knowledge, and investing style.

Successful investing begins long before the Buy button.

The most important decision is not how to place an order.

It is understanding what you are buying and why you are buying it.

In the next lesson, we will explore Mutual Funds and SIP Investing, including how professional fund management works, when SIPs make sense, when lump-sum investing may be appropriate, and how to select investments based on your financial goals rather than recent performance.

Lesson 3: Mutual Funds & SIP Investing

Professional Management, Systematic Investing, and Building Wealth Consistently

Why This Lesson Matters

After learning about stocks and ETFs, many investors arrive at an important realization:

“I don’t have the time, interest, or expertise to analyze companies regularly.”

This is completely normal.

Most people have:

- Careers

- Businesses

- Families

- Responsibilities

They cannot spend hours studying annual reports, earnings calls, and financial statements.

Yet they still want their money to grow.

This is where mutual funds become valuable.

Mutual funds allow investors to participate in financial markets without personally selecting and managing every investment.

For millions of investors, mutual funds provide a practical balance between professional management and long-term wealth creation.

What Is a Mutual Fund?

A mutual fund pools money from thousands of investors.

This pooled money is then managed by professional fund managers according to a specific investment objective.

Instead of buying individual stocks yourself, the fund manager makes investment decisions on behalf of investors.

Think of it this way:

Option A: Do It Yourself

You:

- Research companies

- Analyze financial statements

- Monitor performance

- Make buy and sell decisions

Option B: Professional Management

A professional team performs those tasks for you.

This is essentially how mutual funds work.

A Real-Life Example

Imagine 10,000 investors each contribute money to a mutual fund.

Together, the fund now manages a large pool of capital.

The fund manager may then invest across:

- Large companies

- Mid-sized businesses

- Debt instruments

- International markets

depending on the fund’s objective.

As an investor, you own units of the mutual fund rather than individual securities.

Why Mutual Funds Exist

Many beginners assume mutual funds exist because stock investing is difficult.

That is only partially true.

The real reason is efficiency.

Professional fund managers have access to:

- Research teams

- Industry analysis

- Management meetings

- Financial databases

- Portfolio construction tools

Most retail investors do not.

Mutual funds allow investors to benefit from professional portfolio management without needing to become investment experts themselves.

Understanding Different Types of Mutual Funds

One of the biggest beginner mistakes is searching for:

“Best Mutual Fund”

There is no universal best mutual fund.

The right fund depends on your objective.

Let’s understand the major categories.

Equity Mutual Funds

These funds primarily invest in stocks.

Their goal is long-term growth.

Best For

Investors who:

- Have long investment horizons

- Can tolerate volatility

- Want wealth creation

Example

Suppose your goal is retirement 25 years away.

Short-term market fluctuations become less important.

Long-term growth becomes more important.

Equity funds may become suitable candidates.

Debt Mutual Funds

These funds invest in fixed-income securities such as:

- Bonds

- Treasury Bills

- Corporate Debt

Their primary focus is stability rather than aggressive growth.

Best For

Investors who:

- Need lower volatility

- Have shorter time horizons

- Prioritize capital preservation

Hybrid Mutual Funds

These funds combine:

- Equity

- Debt

within a single portfolio.

Think of them as a middle ground.

Best For

Investors seeking:

- Growth

- Stability

without managing separate allocations themselves.

What Most Beginners Don’t Realize

The best fund category depends on the goal.

Not the recent return.

This is one of the most important concepts in investing.

Example

Goal:

Retirement in 25 years

Potential Solution:

Equity-oriented approach

Goal:

House down payment in 2 years

Potential Solution:

Lower-volatility approach

Notice something important.

The goal changed.

Therefore the investment approach changed.

Understanding SIPs

Now we arrive at one of the most misunderstood concepts in investing.

Many people believe:

SIP is an investment.

It isn’t.

A SIP is simply a method of investing.

The Simplest Explanation

Think about this carefully:

Mutual Fund = Investment

SIP = Method of Investing

A mutual fund is what you invest in.

A SIP is how you invest.

This distinction is critical.

Example

Suppose you invest:

₹5,000 every month

into an equity mutual fund.

The mutual fund is the investment.

The SIP is simply the process used to make recurring contributions.

Why SIPs Became So Popular

SIPs solve a practical problem.

Most people earn money regularly.

Usually every month.

SIPs align investing with income.

Instead of waiting to accumulate a large amount, investors can begin immediately.

Benefits of SIP Investing

Discipline

Investing becomes automatic.

You invest regardless of market headlines.

Consistency

Regular investing builds habits.

Wealth creation often comes from consistency rather than brilliance.

Reduced Timing Pressure

Many investors worry about:

“Is this the right time to invest?”

SIPs reduce this pressure by spreading investments across time.

Emotional Control

Automation reduces the temptation to constantly react to market movements.

SIP vs Lump Sum Investing

One of the most common beginner questions is:

Which is better?

The answer depends on the situation.

SIP Example

Imagine:

Monthly Salary = ₹80,000

Monthly Investment = ₹10,000

A SIP naturally fits this situation.

Money arrives monthly.

Investments occur monthly.

Lump Sum Example

Suppose you receive:

- Annual Bonus

- Inheritance

- Property Sale Proceeds

- Business Exit Proceeds

You already possess the capital.

A lump sum investment becomes a possibility.

Important Insight

This is not necessarily a competition.

Many investors use both.

They invest lump sums when available while maintaining ongoing SIPs.

Common Mutual Fund Mistakes

Chasing Last Year’s Winners

Many investors buy funds simply because they recently performed well.

Past performance alone is rarely enough.

Owning Too Many Funds

Some investors believe:

More funds = More diversification.

Not always.

Sometimes it simply creates complexity.

Switching Frequently

Constantly changing funds often hurts more than it helps.

Investing Without a Goal

The goal should determine the investment.

Not the other way around.

Stopping SIPs During Market Declines

Ironically, many investors stop investing when prices become more attractive.

This is often driven by emotion rather than logic.

A Practical Fund Selection Framework

Before investing in any mutual fund, ask:

What is my goal?

How long can I stay invested?

How much volatility can I tolerate?

Why am I choosing this fund?

Would I still be comfortable holding it during a market decline?

If you cannot answer these questions, more research may be needed.

Direct Plans vs Regular Plans

Another important concept beginners should understand.

Direct Plans

You invest directly with the fund house.

Generally lower expenses.

Regular Plans

Investment occurs through intermediaries or distributors.

Includes advisory and distribution costs.

Important Point

Lower cost does not automatically mean better.

Higher cost does not automatically mean worse.

The right choice depends on:

- Knowledge

- Comfort level

- Need for guidance

However, investors should always understand what they are paying for.

Where Do You Buy Mutual Funds?

Mutual funds can be purchased through:

AMC Websites

Directly from the fund house.

Mutual Fund Platforms

Dedicated investment platforms.

Broker Applications

Many modern brokers support mutual fund investing.

Financial Advisors

For investors seeking guidance.

Unlike ETFs and stocks, a Demat account is generally not required for most mutual fund investments.

This is a major difference that beginners should remember.

Key Takeaway

Mutual funds exist to help investors access professionally managed portfolios without needing to research every investment themselves.

A SIP is not an investment.

It is a method of investing regularly.

The most successful mutual fund investors are often not those who constantly search for the best fund.

They are the ones who:

- Choose investments aligned with their goals

- Invest consistently

- Remain patient

- Avoid emotional decisions

In the next lesson, we will explore Bonds and Debt Investing, understand why stability matters, how bonds generate returns, when they deserve a place in a portfolio, and why many experienced investors use them even when stocks receive most of the attention.

Lesson 4: Bonds & Debt Investing

Understanding Stability, Income, and the Other Side of Investing

Why This Lesson Matters

Ask a beginner about investing and they will usually mention:

- Stocks

- Mutual Funds

- ETFs

Rarely do they talk about bonds.

This is understandable.

Stocks often dominate headlines because they offer the potential for higher returns and exciting growth stories.

Bonds rarely receive the same attention.

Yet many experienced investors, pension funds, insurance companies, and large institutions allocate significant amounts of capital to bonds.

Why?

Because successful investing is not only about maximizing returns.

It is also about managing risk, preserving capital, and creating stability.

This is where bonds play an important role.

Understanding bonds helps investors build more balanced portfolios and make better long-term decisions.

What Is a Bond?

At its simplest, a bond is a loan.

When you buy a stock:

You become an owner.

When you buy a bond:

You become a lender.

This is the most important distinction to remember.

A Simple Example

Imagine a company needs money to expand its business.

Instead of borrowing from a bank, it raises money from investors.

You invest ₹10,000 in its bond.

In return, the company agrees to:

- Pay periodic interest

- Return your original investment at maturity

You are not an owner of the company.

You are a lender.

How Bonds Generate Returns

Most bonds generate returns through interest payments.

This interest is often called a coupon.

Example

Suppose:

Investment Amount = ₹1,00,000

Bond Interest Rate = 8% per year

You may receive:

₹8,000 annually

until maturity.

At maturity, the principal amount is returned according to the bond terms.

Why Bonds Exist

Many investors assume bonds exist only for conservative investors.

That is not entirely true.

Bonds serve several important purposes.

For Governments

Governments issue bonds to:

- Fund infrastructure

- Finance development projects

- Manage public spending

For Companies

Companies issue bonds to:

- Expand operations

- Fund projects

- Raise capital

without giving away ownership.

For Investors

Bonds may provide:

- Regular income

- Lower volatility

- Portfolio stability

- Capital preservation

Types of Bonds Indian Investors May Encounter

While there are many bond categories, beginners should understand the major ones.

Government Bonds

Issued by:

- Government of India

- State Governments

Generally considered among the safest debt instruments because they are backed by government entities.

Best For

Investors prioritizing safety and stability.

Corporate Bonds

Issued by private companies.

These bonds often offer higher interest rates than government bonds.

However:

Higher return usually comes with higher risk.

Example

A financially strong company and a financially weak company may both issue bonds.

The weaker company often needs to offer higher interest rates to attract investors.

This additional return compensates investors for additional risk.

Tax-Free Bonds

Certain bonds may offer tax advantages subject to prevailing regulations.

These are often attractive for specific investor categories.

Always review current tax rules before investing.

What Most Beginners Don’t Realize

A higher interest rate does not automatically mean a better bond.

Often it means:

Higher risk.

This is one of the most important lessons in debt investing.

Understanding Credit Risk

When lending money, one important question must always be asked:

Can the borrower repay?

This is known as credit risk.

Example

Imagine lending money to:

Person A

Stable income

Strong financial position

Person B

Unstable income

Significant financial problems

Most people would consider Person A safer.

Bond investing follows similar logic.

Credit Ratings

To help investors evaluate risk, bonds are often assigned credit ratings.

Examples include:

- AAA

- AA

- A

Generally speaking:

Higher ratings suggest stronger credit quality.

Lower ratings suggest higher risk.

Important Reminder

Ratings are useful.

But they are not guarantees.

Investors should still understand what they own.

Understanding Maturity

Another important bond concept is maturity.

Maturity refers to the date when the principal amount is scheduled to be returned.

Example

A:

2-Year Bond

returns principal after 2 years.

A:

10-Year Bond

returns principal after 10 years.

Why It Matters

Longer maturities may react differently to:

- Interest rates

- Inflation

- Economic conditions

Understanding maturity helps align investments with goals.

The Relationship Between Interest Rates and Bond Prices

This is one of the most important concepts in bond investing.

When interest rates rise:

Existing bond prices often fall.

When interest rates fall:

Existing bond prices often rise.

Why?

Imagine you own a bond paying 6%.

Suddenly new bonds are issued paying 8%.

Most investors would prefer the new bonds.

As a result, the value of older lower-yield bonds may decline.

This relationship is fundamental to bond markets.

When Might Bonds Make Sense?

The answer depends on your goals.

Scenario 1: Capital Preservation

Suppose an investor plans to use money within a few years.

Protecting capital may become more important than maximizing returns.

Scenario 2: Regular Income

Some investors seek predictable cash flows.

Bonds can help support this objective.

Scenario 3: Portfolio Stability

Many experienced investors use bonds to reduce overall portfolio volatility.

A Portfolio Example

Consider two investors.

Investor A

100% Stocks

Portfolio value fluctuates significantly.

Investor B

80% Stocks

20% Bonds

Portfolio may experience lower volatility.

The goal is not necessarily higher returns.

The goal is smoother outcomes.

Common Bond Investing Mistakes

Chasing High Yields

One of the most common mistakes.

Many investors focus only on interest rates.

Remember:

Higher yield often means higher risk.

Ignoring Credit Quality

A bond is only as reliable as the issuer’s ability to repay.

Ignoring Maturity

Investors should understand when money may be needed before committing to long-term investments.

Assuming Bonds Are Risk-Free

All investments involve risk.

Bonds generally carry different risks than stocks, not zero risk.

Where Can You Buy Bonds?

Indian investors can access bonds through:

Stock Exchanges

Certain listed bonds trade on exchanges.

RBI Retail Direct

Allows investors to invest in government securities directly.

Bond Platforms

Dedicated bond investment platforms.

Banks and Financial Institutions

Certain bond offerings may be available through these channels.

A Simple Bond Evaluation Framework

Before investing in any bond, ask:

Who issued it?

What is the credit quality?

What interest rate is offered?

When does it mature?

Why am I investing in it?

If you cannot answer these questions confidently, more research may be required.

Stocks vs Bonds: Understanding the Difference

| Stocks | Bonds |

|---|---|

| Ownership | Lending |

| Higher growth potential | More stable income potential |

| Higher volatility | Generally lower volatility |

| Profits depend on business performance | Returns largely depend on bond terms |

| Long-term wealth creation focus | Stability and income focus |

Neither is universally better.

They serve different purposes.

Key Takeaway

Bonds are not designed to create excitement.

They are designed to provide stability, income, and balance.

When you buy a stock, you become an owner.

When you buy a bond, you become a lender.

Understanding this difference helps investors build portfolios that align with their goals rather than simply chasing returns.

Many successful investors use bonds not because they dislike growth, but because they understand the value of stability.

In the next and final lesson, we will bring everything together by exploring order types, execution mistakes, risk controls, and the practical lessons that can help investors avoid costly errors when placing investment orders.

Lesson 5: Order Types, Execution Mistakes & Risk Controls

How Smart Investors Avoid Costly Errors Before and After Placing an Order

Why This Lesson Matters

After understanding:

- Stocks

- ETFs

- Mutual Funds

- SIPs

- Bonds

most investors feel ready to begin.

However, there is one final area that deserves attention.

Execution.

The difference between a successful investment and an avoidable mistake often comes down to a few simple decisions made before placing an order.

Many investors spend hours researching investments but only seconds reviewing their actual orders.

Unfortunately, those few seconds can sometimes become expensive.

This lesson will help you understand:

- How order types work

- When to use them

- Common execution mistakes

- Risk-control principles

- Practical habits that can improve decision-making

Because successful investing is not only about choosing good investments.

It is also about executing decisions correctly.

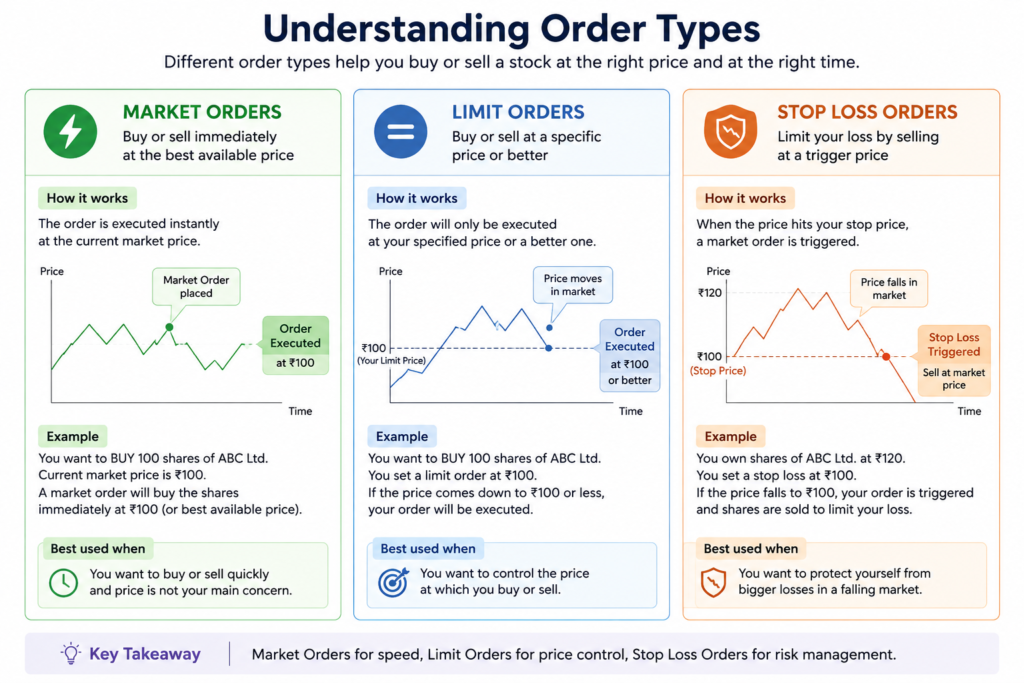

Understanding Order Types

When placing an order through a broker, investors usually encounter different order options.

The most common are:

Market Orders, Limit Orders and Stop Loss Orders

Understanding when to use each can prevent unnecessary mistakes.

Market Orders

A market order tells the broker:

“Execute my order immediately at the best available price.”

Speed is the priority.

Price certainty is not.

Example

Suppose a stock is currently trading at:

₹1,000

You place a market order.

If the price changes quickly, your order may execute at:

- ₹1,001

- ₹1,003

- ₹1,005

or another nearby price.

Execution happens quickly.

But you do not control the final execution price.

Best Used When

- Liquidity is high

- Immediate execution is important

- Small price differences are not critical

Potential Risk

Investors sometimes assume market orders guarantee the displayed price.

They do not.

They guarantee execution, not price.

Limit Orders

A limit order allows you to specify the maximum price you are willing to pay.

Price control becomes the priority.

Example

Current Price:

₹1,000

You place a limit order at:

₹995

Two outcomes are possible.

Scenario A

Price falls to ₹995.

Order executes.

Scenario B

Price never reaches ₹995.

Order remains pending.

Important Trade-Off

Market Order

= Higher execution certainty

= Less price control

Limit Order

= Greater price control

= Less execution certainty

Which Order Type Should Beginners Use?

There is no universal answer.

However:

For highly liquid investments such as large ETFs and major stocks, either approach may be reasonable depending on circumstances.

The key is understanding the trade-off.

Never select an order type without knowing what it does.

Stop Loss Orders

A stop loss is designed to limit potential losses.

Think of it as a predefined exit plan.

Example

Purchase Price:

₹1,000

Stop Loss:

₹900

If the price falls to the specified level, the order may trigger automatically according to the order conditions.

Why Investors Use Stop Losses

Stop losses help reduce emotional decision-making.

Instead of making decisions during panic, rules are established beforehand.

Important Reality

A stop loss is not a guarantee.

In rapidly moving markets, actual execution may differ from the exact stop price.

Investors should understand this limitation.

What Most Long-Term Investors Should Know

Many beginners assume:

Every investment requires a stop loss.

Not necessarily.

A trader and a long-term investor often have different objectives.

Example

A trader holding positions for hours or days may rely heavily on stop losses.

A long-term investor owning a business for ten years may focus more on business fundamentals than daily price movements.

Context matters.

The Most Common Execution Mistakes

Let’s move beyond order types and discuss the mistakes that actually cost investors money.

Mistake #1: Buying Without Understanding

This remains the most expensive mistake.

Investors buy because:

- Someone recommended it

- Social media is discussing it

- The price recently increased

Without understanding the investment itself.

Better Question

Before buying, ask:

“Can I explain this investment in simple language?”

If not, more research may be required.

Mistake #2: Entering the Wrong Quantity

This sounds simple.

Yet it happens surprisingly often.

A misplaced digit can significantly change the size of an investment.

Example

Intended Quantity:

10 shares

Entered Quantity:

100 shares

A simple mistake can create an entirely different exposure.

Always review orders carefully.

Mistake #3: Investing Everything at Once

Many beginners become excited after learning about investing.

They rush to deploy all available capital immediately.

Patience is often a better strategy.

A Better Approach

Build experience gradually.

Confidence should come from understanding, not enthusiasm.

Mistake #4: Confusing Investing with Trading

This mistake creates enormous confusion.

Investors begin with long-term intentions.

Then start reacting to daily price movements.

Soon they are behaving like traders without possessing trading skills.

Ask Yourself

Am I:

- Investing for years?

- Trading for short-term movements?

The answer should guide your decisions.

Mistake #5: Ignoring Costs

Every transaction may involve costs.

Examples include:

- Brokerage

- Taxes

- Exchange charges

- Other fees

Individually they may appear small.

Over time they can accumulate.

Investors should always understand the costs associated with their activities.

Mistake #6: Chasing Prices

Many investors feel comfortable buying only after prices rise.

Ironically, this often means enthusiasm increases after opportunities become more expensive.

Price movement alone should never become the investment thesis.

A Simple Risk-Control Framework

Before placing any order, ask:

What am I buying?

Why am I buying it?

What could go wrong?

How much am I investing?

How long do I plan to hold it?

Would I still be comfortable if prices decline temporarily?

These six questions can prevent many avoidable mistakes.

The 24-Hour Rule

One useful habit for beginners:

If you suddenly feel excited about an investment opportunity, wait 24 hours before acting.

This simple pause often reveals:

- Missing information

- Emotional decisions

- Overlooked risks

Great opportunities usually remain available tomorrow.

Poor decisions often begin today.

Building Good Investing Habits

Successful investors rarely rely on luck.

They build systems.

Examples:

✔ Research before investing

✔ Review orders carefully

✔ Understand what they own

✔ Stay diversified

✔ Focus on long-term goals

✔ Learn continuously

These habits may seem ordinary.

Over decades, they become powerful advantages.

Bringing Everything Together

By now you understand:

Stocks

Direct ownership of businesses.

ETFs

Diversified baskets traded like stocks.

Mutual Funds

Professionally managed portfolios.

SIPs

A method of investing regularly.

Bonds

Loans that provide stability and income potential.

Order Types

Tools that help execute investment decisions.

Each serves a different purpose.

The best investors understand not only what to buy but also how and why they are buying it.

Cherry on Top: Managing Multiple Demat Accounts

Many investors eventually end up with multiple Demat accounts because they:

- Change brokers

- Test new platforms

- Forget to close old accounts

Over time, tracking holdings can become difficult.

A useful solution is the MyEasi facility from the Central Depository Services Limited, which allows eligible investors to view holdings, transactions, and statements across grouped Demat accounts under a single login.

This is a small tip that can save significant time as your investing journey grows.

Final Advice

If there is one lesson worth remembering from this entire section, it is this:

Investing is not a race.

Many beginners feel pressure to:

- Find the perfect stock

- Start immediately

- Maximize returns

- Beat everyone else

The market does not reward urgency.

It rewards discipline.

You do not need to know everything before investing.

But you should understand what you are doing and why you are doing it.

Start small.

Stay curious.

Keep learning.

Allow time to work in your favour.

Because in investing, consistency often beats brilliance.

Key Takeaway

Great investing is not about placing perfect orders.

It is about making thoughtful decisions, avoiding unnecessary mistakes, and following a process you can repeat for years.

Order types, risk controls, and execution tools are important.

But the most valuable investing skill remains good judgment.

Technology will evolve.

Markets will change.

New opportunities will emerge.

The ability to think clearly and act patiently will always remain one of an investor’s greatest advantages.

Bonus Lesson: Knowing When to Hold, Stop, or Exit an Investment

One of the Most Important Investing Questions

Most investors spend a lot of time learning:

- What to buy

- When to buy

- How much to buy

Very few spend enough time thinking about:

When should I stop, redeem, or exit an investment?

Successful investing is not only about entering investments wisely. It is also about knowing when an investment has completed its job.

The answer depends on why you invested in the first place.

Stocks

Consider Reviewing or Exiting When:

✔ The business fundamentals deteriorate significantly.

✔ Management quality becomes questionable.

✔ The original investment thesis is no longer valid.

✔ Better opportunities exist for your capital.

✔ The company no longer fits your investment strategy.

Avoid Selling Solely Because:

✘ The stock price fell temporarily.

✘ Negative news created short-term fear.

✘ Others are selling.

A falling stock price and a weakening business are not always the same thing.

ETFs

Consider Exiting When:

✔ Your financial goal has been achieved.

✔ Portfolio rebalancing is required.

✔ You need funds for another objective.

✔ The ETF no longer aligns with your investment strategy.

Avoid Exiting Because:

✘ Markets experienced a temporary correction.

✘ Short-term returns disappointed you.

ETFs are generally designed for long-term participation rather than constant buying and selling.

Mutual Funds

Consider Reviewing or Redeeming When:

✔ Your financial goal is achieved.

✔ The fund’s investment strategy changes significantly.

✔ Long-term performance consistently disappoints expectations relative to its category.

✔ Your risk tolerance changes.

✔ Portfolio rebalancing becomes necessary.

Avoid Redeeming Because:

✘ One year of weak returns.

✘ Temporary market declines.

✘ Short-term underperformance.

Many investors damage long-term returns by constantly switching between funds.

SIPs

Consider Stopping a SIP When:

✔ The financial goal has been fully funded.

✔ The underlying fund is no longer suitable.

✔ Asset allocation adjustments are needed.

✔ Major life circumstances require a new investment plan.

Avoid Stopping a SIP Because:

✘ Markets are falling.

✘ News headlines are negative.

✘ Fear has increased.

Some of the best long-term investing opportunities often appear during difficult market periods.

Bonds

Consider Exiting When:

✔ Funds are required for a planned objective.

✔ Credit quality deteriorates significantly.

✔ Your portfolio requirements change.

✔ Better fixed-income alternatives become available.

Remember

Higher yields often come with higher risk.

Always understand why a bond offers a particular return.

The Most Important Exit Question

Before selling any investment, ask:

Has the reason I bought this investment changed?

If the answer is:

No

You may need a stronger reason to sell.

If the answer is:

Yes

A review may be justified.

This simple question can prevent many emotional decisions.

Final Takeaway

Stocks

For ownership and long-term wealth creation.

ETFs

For diversification and passive investing.

Mutual Funds

For professional management and goal-based investing.

SIPs

For disciplined and consistent investing.

Bonds

For stability, income, and portfolio balance.

The Golden Principle

Buy because of a reason. Hold because the reason remains valid. Exit when the reason changes or the goal is achieved.

Many investing mistakes happen because investors buy without a plan and sell without a reason.

Having both is one of the simplest ways to become a better investor.

Suggested Gutenberg Card Format

📚 Learn About Mutual Funds & SIPs

Understand SIPs, fund categories, risk levels, and long-term wealth creation.

External Resource: https://www.amfiindia.com/ https://www.amfiindia.com/

📚 Learn About Bonds & Fixed Income https://ncfe.org.in/

Explore government bonds, corporate bonds, debt funds, yields, and interest rate risks.

External Resource: SEBI https://investor.sebi.gov.in/

Next Explore