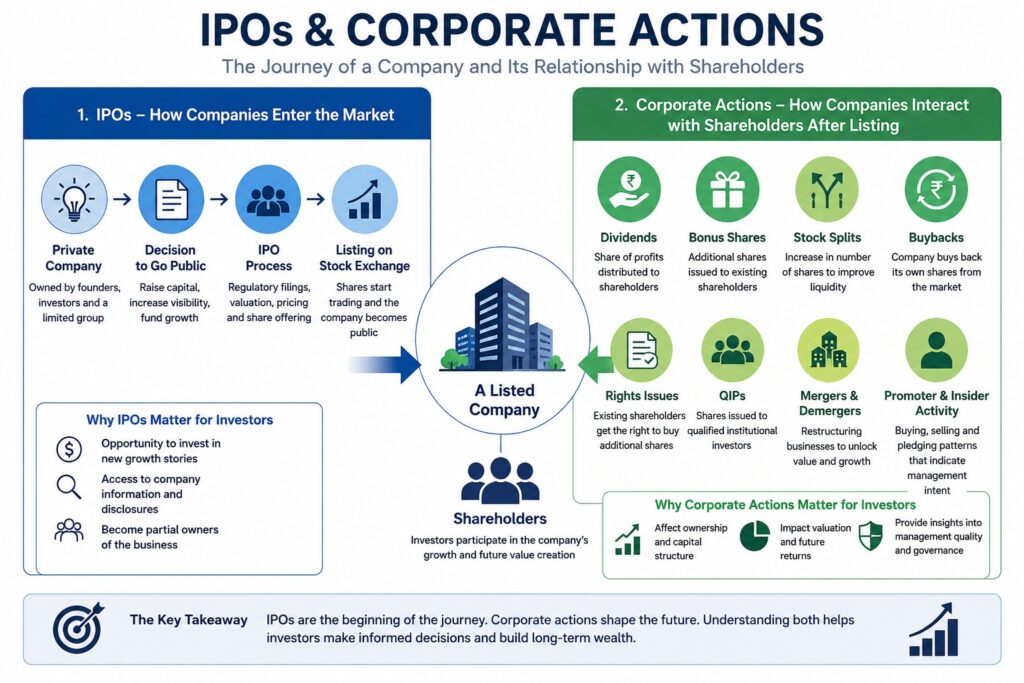

IPOs & Corporate Actions

A company’s relationship with the stock market does not begin and end with its share price.

Every listed company follows a journey. It first enters the stock market through an Initial Public Offering (IPO), allowing public investors to participate in its future growth. Once listed, the company continues to make important decisions that affect shareholders, ownership structure, capital allocation, and long-term value creation. These decisions are known as corporate actions.

Understanding both IPOs and corporate actions is important because they help investors answer two fundamental questions:

How does a company enter the stock market?

and

How does a company interact with shareholders after listing?

The IPO process helps investors understand why companies go public, how shares are offered to the public, how IPOs are priced, and how investors should evaluate new listings.

Corporate actions help investors understand why companies pay dividends, issue bonus shares, conduct stock splits, raise additional capital, buy back shares, restructure businesses, or change ownership patterns.

While IPOs represent the beginning of a company’s public market journey, corporate actions shape the relationship between the company and its shareholders throughout the years that follow.

Together, these topics provide valuable insight into how businesses raise capital, allocate resources, reward shareholders, restructure operations, and create long-term value.

What We Will Cover

IPOs

- Understanding IPOs

- The IPO Journey

- How to Analyze an IPO

- IPO Risks, Lock-Ins & Investor Psychology

Corporate Actions

- Dividends, Bonus Shares & Stock Splits

- Buybacks, Rights Issues & QIPs

- Mergers, Demergers & Corporate Restructuring

- Promoters, Insider Activity & Corporate Signals

By the end of this section, you will understand not only how companies enter the stock market, but also how management decisions continue to influence shareholders long after the listing day.

Lesson 1: Understanding IPOs – How Companies Enter the Stock Market

Every company starts as a private business.

In the early stages, founders typically fund the business using their own savings, contributions from family and friends, bank loans, private investors, venture capital firms, or private equity funds.

As the business grows, its capital requirements often increase. Expansion may require new factories, technology investments, acquisitions, research and development, debt reduction, or working capital. At this stage, companies may seek access to a much larger pool of capital through the stock market.

This process is known as an Initial Public Offering (IPO).

An IPO marks the transition of a company from private ownership to public ownership.

What Is an IPO?

An Initial Public Offering (IPO) is the process through which a private company offers its shares to the public for the first time and becomes a publicly listed company.

Before an IPO, ownership is generally limited to:

- Founders

- Promoters

- Early investors

- Venture capital firms

- Private equity funds

- Employees holding stock options

After an IPO, public investors can also become shareholders by purchasing shares in the company.

In simple terms, an IPO allows investors to participate in the future growth of a business while providing the company access to public capital markets.

Why Do Companies Go Public?

Companies pursue IPOs for various reasons.

Raising Growth Capital

One of the most common reasons is raising money for future expansion.

The funds may be used for:

- Business expansion

- New manufacturing facilities

- Research and development

- Technology investments

- Acquisitions

- Working capital requirements

Access to public capital can help accelerate growth plans.

Reducing Debt

Some companies use IPO proceeds to repay existing borrowings.

Lower debt may:

- Reduce interest costs

- Improve financial stability

- Strengthen the balance sheet

Providing Exit Opportunities

Early investors such as venture capital and private equity funds often invest years before an IPO.

An IPO provides a pathway for these investors to partially or fully monetize their investment.

Improving Visibility and Credibility

Listed companies often receive greater attention from:

- Investors

- Customers

- Suppliers

- Lenders

- Financial institutions

Public listing can enhance a company’s visibility and reputation.

Fresh Issue vs Offer for Sale (OFS)

Not all IPOs are structured in the same way.

Understanding this distinction is important.

Fresh Issue

In a fresh issue, the company creates new shares and sells them to investors.

The money raised goes directly to the company.

Example:

A company issues new shares worth ₹1,000 crore.

The ₹1,000 crore is received by the company and can be used for business purposes.

Offer for Sale (OFS)

In an Offer for Sale, existing shareholders sell part of their holdings.

The company does not receive the proceeds.

Instead, the money goes to the selling shareholders.

These sellers may include:

- Promoters

- Venture capital firms

- Private equity investors

- Early investors

Why This Difference Matters

Suppose two companies each launch a ₹1,000 crore IPO.

Company A:

- ₹1,000 crore Fresh Issue

Company B:

- ₹1,000 crore OFS

Although both IPOs are the same size, their purpose is very different.

Company A is raising capital for growth.

Company B is primarily providing an exit opportunity to existing shareholders.

This is one of the first things investors should examine when evaluating an IPO.

What Changes After an IPO?

Once listed, a company enters a very different environment.

It must:

- Follow regulatory requirements

- Disclose financial results regularly

- Report material developments

- Maintain transparency with shareholders

Ownership also becomes widely distributed among public investors.

The company is now accountable not only to promoters but also to thousands of shareholders.

Benefits of Going Public

For Companies

- Access to capital

- Improved visibility

- Increased credibility

- Liquidity for shareholders

- Acquisition currency through shares

For Investors

- Opportunity to participate in business growth

- Access to previously private companies

- Potential long-term wealth creation

Going Public Does Not Guarantee Success

A common misconception is that every IPO represents a great investment opportunity.

In reality:

- Some IPOs perform exceptionally well.

- Some generate modest returns.

- Some decline significantly after listing.

The success of an IPO ultimately depends on:

- Business quality

- Financial performance

- Industry conditions

- Valuation

- Execution after listing

An IPO should therefore be viewed as the beginning of the investment evaluation process, not the end of it.

Key Takeaways

- An IPO is the process through which a private company becomes publicly listed.

- Companies go public to raise capital, reduce debt, provide exits to investors, and enhance visibility.

- Fresh Issue raises money for the company, while OFS allows existing shareholders to sell their holdings.

- Public listing increases transparency and shareholder participation.

- Not all IPOs are attractive investments.

- Investors should understand why a company is going public before deciding whether to invest.

Lesson 2: The IPO Journey – From Private Company to Listed Company

When investors see an IPO open for subscription, most of the hard work has already been completed.

The journey from a private company to a publicly listed company is often a long and highly regulated process involving multiple participants, extensive disclosures, regulatory reviews, and investor engagement.

Understanding this process helps investors appreciate how companies enter public markets and why IPO documents contain so much information.

The Decision to Go Public

The IPO journey begins when a company’s management and promoters decide that public markets are the appropriate next step for the business.

This decision may be driven by:

- Expansion plans

- Capital requirements

- Debt reduction

- Investor exits

- Increased visibility

Once this decision is made, the company begins preparing for the listing process.

Appointing Key Advisors

A company cannot simply decide to list its shares and immediately approach investors.

Several professional advisors are involved.

Merchant Bankers

Merchant bankers (also called lead managers) play a central role in the IPO process.

Their responsibilities include:

- Managing the IPO process

- Coordinating with regulators

- Preparing offer documents

- Assisting with pricing

- Marketing the issue

They act as a bridge between the company, regulators, and investors.

Other Participants

The process may also involve:

- Legal advisors

- Auditors

- Registrars

- Bankers

- Compliance professionals

Each participant helps ensure that regulatory requirements are met.

Preparing the DRHP

One of the most important documents in the IPO process is the Draft Red Herring Prospectus (DRHP).

This document provides detailed information about:

- The business

- Industry overview

- Financial statements

- Promoters

- Management

- Risks

- Use of IPO proceeds

- Shareholding structure

For investors, the DRHP is one of the most valuable sources of information when evaluating an IPO.

Regulatory Review

After the DRHP is submitted, regulators review the document.

The objective is not to determine whether the business is a good investment.

Instead, regulators focus on:

- Accuracy of disclosures

- Compliance requirements

- Transparency

- Investor protection

Companies may be required to provide additional clarifications before proceeding.

Roadshows and Investor Meetings

Before the IPO opens, management teams often interact with institutional investors.

These meetings help:

- Explain the business model

- Discuss growth opportunities

- Address investor concerns

- Generate interest in the offering

Institutional participation often plays an important role in the IPO process.

Price Band and Book Building

Most modern IPOs use a book-building process.

Instead of announcing a fixed price immediately, the company provides a price range known as the price band.

Example

Price Band:

₹450 – ₹500 per share

Investors submit bids within this range.

Based on investor demand, the final issue price is determined.

This process helps discover a market-driven price for the offering.

Subscription Period

Once the IPO opens, investors can submit applications.

Different categories participate in the offering:

Retail Investors

Individual investors applying within the retail category.

Qualified Institutional Buyers (QIBs)

Large institutional investors such as:

- Mutual Funds

- Insurance Companies

- Pension Funds

Non-Institutional Investors (NIIs)

High-net-worth investors and larger applicants.

The level of subscription often becomes a closely watched indicator during the IPO process.

Allotment of Shares

After the subscription period closes, shares are allocated to successful applicants.

When demand exceeds available shares, investors may receive:

- Partial allotment

- Minimum allotment

- No allotment

Oversubscription does not guarantee future performance, but it often attracts significant attention from investors.

Listing Day

After allotment is completed, the company’s shares begin trading on the stock exchange.

This is known as the listing.

The market now determines the share price based on:

- Demand and supply

- Investor expectations

- Valuation perceptions

- Market conditions

From this point onward, the company becomes a publicly traded business.

The IPO Journey Does Not End at Listing

Many investors treat listing day as the end of the IPO process.

In reality, listing day is merely the beginning.

Once public, the company must:

- Report financial results regularly

- Communicate with shareholders

- Comply with disclosure requirements

- Deliver on business expectations

Long-term investment success depends far more on business execution than on listing-day performance.

Why Investors Should Understand the Process

Understanding the IPO process helps investors:

- Read offer documents more effectively

- Evaluate management disclosures

- Interpret subscription data properly

- Understand how issue pricing works

- Make more informed investment decisions

The IPO process is designed to help companies access public capital while providing investors with information needed to evaluate opportunities.

Key Takeaways

- The IPO journey begins long before investors can apply for shares.

- Merchant bankers, auditors, legal advisors, and regulators all play important roles.

- The DRHP is one of the most important documents for IPO analysis.

- Most IPOs use a book-building process to determine pricing.

- Investors participate through retail, institutional, and non-institutional categories.

- Listing day marks the beginning of a company’s public market journey, not the end.

- Understanding the IPO process helps investors evaluate offerings more effectively.

Lesson 3: How to Analyze an IPO

Every IPO presents a story.

Management discusses future opportunities, industry growth, competitive strengths, and expansion plans. Investors are often presented with attractive narratives and optimistic projections.

However, successful IPO investing requires looking beyond the story.

The key question is not:

“Is this a good company?”

The key question is:

“Is this a good investment at this price?”

Understanding this difference is critical.

A great company can be a poor investment if investors pay too much for it, while a modest business can generate attractive returns if purchased at a reasonable valuation.

Step 1: Understand the Business

Before looking at financials or valuations, investors should understand how the company makes money.

Questions worth asking include:

- What products or services does the company provide?

- Who are its customers?

- How does it generate revenue?

- What makes it different from competitors?

- Is the business easy to understand?

If investors cannot explain the business in simple language, they probably do not understand it well enough to invest.

Example

Consider two companies:

Company A manufactures automobile components.

Company B operates in a highly specialized technology niche that investors struggle to understand.

In many cases, investing in a business you understand may be safer than investing in a business that merely sounds exciting.

Step 2: Examine Why the Company Is Raising Money

One of the first sections investors should review is the use of proceeds.

Ask:

Why is the company coming to the market?

Possible reasons include:

- Capacity expansion

- New projects

- Debt reduction

- Acquisitions

- Working capital requirements

These are often growth-oriented uses of capital.

Investors should be more cautious when a large portion of the IPO consists of existing shareholders exiting through an Offer for Sale (OFS).

Example

Suppose two companies launch identical ₹2,000 crore IPOs.

Company A:

- ₹1,800 crore Fresh Issue

- ₹200 crore OFS

Company B:

- ₹100 crore Fresh Issue

- ₹1,900 crore OFS

The purpose of these IPOs is very different.

Company A is primarily raising money for the business.

Company B is primarily facilitating shareholder exits.

Neither is automatically good or bad, but investors should understand the difference.

Step 3: Evaluate the Industry

Even a strong company can face challenges if its industry is struggling.

Investors should ask:

- Is the industry growing?

- What are the major risks?

- Is competition increasing?

- Are there long-term tailwinds?

Example

A company operating in a rapidly growing industry may benefit from industry expansion even if it is not the market leader.

Conversely, an excellent company operating in a declining industry may face headwinds.

Step 4: Study the Financials

Financial statements help investors understand the economic reality behind the business.

Key areas to review include:

Revenue Growth

Is the business growing consistently?

Profitability

Is the company generating profits?

If not, is there a clear path toward profitability?

Debt Levels

Does the company have excessive leverage?

Cash Flow

Is cash generation consistent with reported profits?

Strong businesses often demonstrate improvement across multiple financial metrics rather than relying on a single positive number.

Step 5: Assess Management and Promoters

Investors are not only investing in a business.

They are also investing in the people running it.

Questions worth asking include:

- Who are the promoters?

- What is their track record?

- Have they built successful businesses before?

- Do they continue to maintain meaningful ownership after the IPO?

Management quality can influence business performance for many years after listing.

Step 6: Understand Valuation

One of the most overlooked aspects of IPO investing is valuation.

A company may be excellent.

Its industry may be attractive.

Its financials may be strong.

Yet the IPO can still be expensive.

Investors should compare the company’s valuation with:

- Listed competitors

- Industry averages

- Growth prospects

- Profitability

The objective is not to find the cheapest company.

The objective is to determine whether the price being offered is reasonable relative to the business quality.

Step 7: Read the Risk Factors

Most investors skip the risk section of the prospectus.

This is often a mistake.

Risk disclosures may highlight:

- Customer concentration

- Regulatory risks

- Litigation

- Dependence on key suppliers

- Industry challenges

- Business vulnerabilities

Understanding what can go wrong is just as important as understanding what can go right.

Avoid Common IPO Traps

Many investors make decisions based on:

- Oversubscription numbers

- Social media excitement

- News headlines

- Grey market premiums

These factors may influence short-term sentiment but do not determine long-term business performance.

The quality of the business and the price paid remain far more important.

A Simple IPO Analysis Framework

Before investing in any IPO, ask:

Business

Do I understand how the company makes money?

Purpose

Why is the company raising capital?

Industry

Is the industry attractive?

Financials

Are revenue, profits, and cash flows healthy?

Management

Do I trust the people running the business?

Valuation

Am I paying a reasonable price?

Risks

What could go wrong?

The more convincing the answers, the stronger the investment case.

Key Takeaways

- IPO investing begins with understanding the business, not the stock price.

- Investors should examine how IPO proceeds will be used.

- Industry conditions often influence future performance.

- Financials, management quality, and valuation are critical factors.

- Reading risk disclosures is an important part of analysis.

- Oversubscription and market excitement should not replace fundamental evaluation.

- A good company is not automatically a good investment if the valuation is unreasonable.

Lesson 4: IPO Risks, Investor Psychology & Common Mistakes

IPOs often generate excitement that few other market events can match.

News coverage increases, subscription numbers are discussed daily, social media becomes active, and investors begin speculating about listing gains long before the stock starts trading.

While some IPOs become successful long-term investments, others struggle after listing despite strong investor enthusiasm.

Understanding the risks associated with IPO investing is just as important as understanding the opportunity.

The Excitement Trap

Many investors assume that if an IPO is receiving widespread attention, it must be a good investment.

In reality, popularity and investment quality are not the same thing.

Markets often become most excited when expectations are already extremely high.

The problem is that future success depends on a company exceeding expectations, not simply meeting them.

A highly anticipated IPO can still disappoint investors if growth falls short of what the market expected.

Oversubscription Does Not Guarantee Success

One of the most common misconceptions is:

“If an IPO is heavily subscribed, it must be a good investment.”

Oversubscription simply means demand exceeded the number of shares available.

It does not guarantee:

- Strong fundamentals

- Attractive valuation

- Long-term returns

History has shown examples of highly oversubscribed IPOs that later underperformed, as well as modestly subscribed IPOs that generated strong long-term returns.

Demand and business quality are not always the same thing.

The Listing Gain Mindset

Many investors focus entirely on listing day.

Questions often include:

- Will the stock list at a premium?

- How much profit can be made on listing day?

- What is the expected listing gain?

While listing gains can occur, they should not be confused with investing.

A company that lists at a premium may later underperform.

A company that lists quietly may eventually become a successful long-term investment.

Investors should understand whether they are pursuing:

- Short-term listing gains

- Long-term business ownership

The analysis required for each approach is very different.

The Grey Market Premium (GMP) Trap

Grey Market Premiums often attract significant attention before IPO listings.

Many investors treat GMP as a prediction of future returns.

However, GMP:

- Is unofficial

- Is not regulated

- Changes frequently

- Reflects short-term sentiment

While GMP may provide insight into market expectations, it should never replace business analysis.

A strong GMP does not guarantee long-term success.

Understanding Lock-In Periods

One of the most overlooked IPO risks is the lock-in period.

Certain shareholders are restricted from selling immediately after listing.

These may include:

- Promoters

- Anchor Investors

- Private Equity Funds

- Venture Capital Investors

- Pre-IPO Shareholders

After the lock-in period expires, these investors may become eligible to sell their holdings.

Why Does This Matter?

Imagine a company where:

- Only a small portion of shares are actively trading.

- A large number of shares remain under lock-in.

When those restrictions expire, additional shares may enter the market.

This increase in supply can sometimes create pressure on stock prices.

Understanding Investor Exits

Not all selling after a lock-in expiry is negative.

Consider this example:

A private equity investor invested in a company five years before the IPO at an effective cost of ₹100 per share.

The company later lists at ₹800.

Even if the business remains strong, the investor may choose to sell after the lock-in period because the original investment objective has already been achieved.

The sale may reflect portfolio management rather than concerns about the company.

Understanding who owns the shares and why they may sell is often more important than simply observing the sale itself.

Market Conditions Matter

A strong business can still struggle if market conditions are unfavorable.

Similarly, average businesses can sometimes receive strong investor interest during bullish market environments.

IPO performance is often influenced by:

- Market sentiment

- Liquidity conditions

- Interest rates

- Economic outlook

- Investor confidence

This is one reason IPO results vary significantly across market cycles.

The Story vs Reality Problem

Every IPO has a story.

The story may involve:

- Industry growth

- Market opportunities

- Future expansion

- Competitive advantages

Stories attract investors.

Financial performance ultimately determines long-term outcomes.

Investors should ensure that business fundamentals support the narrative being presented.

A Practical IPO Risk Checklist

Before investing in any IPO, ask:

- Am I investing because of the business or because of market excitement?

- Is the valuation reasonable?

- Who is selling shares?

- What is the lock-in structure?

- Are private equity investors likely to exit later?

- What are the major business risks?

- Am I seeking listing gains or long-term ownership?

These questions can help investors avoid some of the most common IPO mistakes.

Key Takeaways

- Popularity and investment quality are not the same thing.

- Oversubscription does not guarantee future returns.

- Listing gains and long-term investing require different approaches.

- GMP reflects sentiment, not business quality.

- Lock-in expiries can affect supply and stock performance.

- Investor exits do not automatically indicate business weakness.

- Market conditions influence IPO outcomes.

- Successful IPO investing requires discipline, analysis, and realistic expectations.

Corporate Actions

Introduction

Once a company becomes publicly listed, its interaction with shareholders does not end. Companies continue to make decisions that can affect ownership structure, capital allocation, liquidity, and shareholder returns. These decisions are known as corporate actions.

Understanding corporate actions helps investors interpret important events and avoid common misconceptions. While some corporate actions change the number of shares outstanding, others return capital to shareholders, raise additional funds, or restructure the business itself.

The key point is that corporate actions often change how value is distributed, but they do not automatically create value. Long-term shareholder wealth is ultimately driven by business performance rather than corporate announcements alone.

Lesson 5: Dividends, Bonus Shares & Stock Splits – Reward, Signal, or Optics?

After a company becomes publicly listed, management continues to make decisions that affect shareholders. Some of these decisions involve distributing profits, increasing the number of shares outstanding, or improving stock liquidity.

Among the most common corporate actions are:

- Dividends

- Bonus Shares

- Stock Splits

These actions often generate excitement among investors. However, many investors misunderstand their purpose and overestimate their impact.

The key question is not:

“What corporate action has been announced?”

The more important question is:

“Why is management doing this, and what does it mean for shareholders?”

Understanding this difference can help investors separate meaningful signals from market excitement.

Dividends: Sharing Profits with Shareholders

A dividend is a portion of a company’s profits distributed to shareholders.

When a company generates cash beyond its operational and growth requirements, management may choose to return some of that cash to investors.

Example

Suppose a company declares:

₹10 dividend per share

An investor holding:

1,000 shares

would receive:

₹10,000

before applicable taxes.

Why Do Companies Pay Dividends?

Not all companies pay dividends.

A young, rapidly growing company may prefer to reinvest profits into expansion.

A mature company with stable cash flows may have fewer opportunities to deploy excess capital productively.

In such situations, returning cash to shareholders may be the most efficient choice.

Dividend-paying companies are often:

- Established businesses

- Market leaders

- Cash-generating companies

- Businesses with predictable earnings

What Does a Dividend Signal?

Dividends often signal:

- Financial stability

- Consistent profitability

- Strong cash generation

However, investors should not assume that a higher dividend automatically means a better company.

Sometimes companies maintain dividends to preserve investor confidence even when business conditions are deteriorating.

The dividend should always be evaluated alongside the company’s financial performance.

Does a Dividend Create Wealth?

A common misconception is that dividends are “free money.”

They are not.

Example

Suppose:

Share Price = ₹500

Dividend = ₹10

After the ex-dividend date, the share price may adjust to approximately:

₹490

The shareholder now owns:

- A ₹490 share

- ₹10 in cash

The form of value changes.

The total value remains broadly similar.

This is why investors should focus on the quality of the business rather than chasing dividends alone.

Bonus Shares: More Shares, Same Business

A bonus issue occurs when a company distributes additional shares to existing shareholders free of cost.

No money changes hands.

Instead, the company converts a portion of its reserves into share capital.

Example: 1:1 Bonus

Suppose an investor owns:

100 shares

The company announces a:

1:1 Bonus Issue

The investor now owns:

200 shares

without investing any additional money.

Why Do Companies Issue Bonus Shares?

Management may issue bonus shares to:

- Increase liquidity

- Improve trading participation

- Reward long-term shareholders

- Signal confidence in the business

However, investors should remember:

A bonus issue does not improve profits.

It does not improve cash flow.

It does not improve the business itself.

Only the share structure changes.

Does a Bonus Make You Richer?

No.

Example

Before Bonus:

100 Shares × ₹1,000 = ₹1,00,000

After 1:1 Bonus:

200 Shares × ₹500 = ₹1,00,000

The number of shares doubles.

The share price adjusts.

The overall value remains broadly unchanged.

This is why bonus announcements should not be confused with wealth creation.

Stock Splits: Making Shares More Accessible

A stock split increases the number of shares by dividing existing shares into smaller units.

Unlike a bonus issue, company reserves are not used.

Only the face value and number of shares change.

Example: 1 Share Becomes 5 Shares

Before Split:

100 Shares × ₹1,000

After Split:

500 Shares × ₹200

Total value remains unchanged.

Why Do Companies Split Shares?

Stock splits are often undertaken when share prices become very high.

Management may want to:

- Improve liquidity

- Increase participation

- Make shares appear more affordable

Although nothing changes fundamentally, lower share prices sometimes attract greater market interest.

Stock Split vs Bonus Issue

Many investors confuse the two.

| Feature | Bonus Issue | Stock Split |

|---|---|---|

| Additional Shares Issued | Yes | Yes |

| Uses Company Reserves | Yes | No |

| Share Price Adjusts | Yes | Yes |

| Immediate Wealth Creation | No | No |

| Business Fundamentals Change | No | No |

Both actions increase the number of shares.

Neither automatically creates value.

Who Actually Benefits?

This is the question investors should always ask.

Dividends

Primary Benefit:

- Existing Shareholders

Bonus Shares

Primary Benefit:

- Liquidity

- Trading Participation

Stock Splits

Primary Benefit:

- Market Accessibility

- Liquidity

In all three cases, the underlying business remains the primary driver of long-term returns.

Green Flags vs Red Flags

Positive Signs

✓ Consistent dividends supported by profits

✓ Bonus issues backed by strong reserves

✓ Stock splits in businesses with strong fundamentals

✓ Management communicating clearly with shareholders

Warning Signs

⚠ Dividend payouts despite weak cash flows

⚠ Excessive focus on corporate actions while business performance deteriorates

⚠ Investors becoming excited about bonus issues while ignoring fundamentals

⚠ Treating stock splits as wealth creation events

The Most Important Lesson

Many investors become excited when companies announce:

- Dividends

- Bonus Shares

- Stock Splits

However, these events do not create value on their own.

Long-term shareholder wealth is created by:

- Revenue Growth

- Profit Growth

- Strong Cash Flows

- Competitive Advantages

- Good Capital Allocation

Corporate actions can influence how value is distributed.

The business itself determines how much value exists in the first place.

Key Takeaways

- Dividends distribute a portion of profits to shareholders.

- Bonus shares increase the number of shares but do not increase ownership value.

- Stock splits improve liquidity by reducing the price per share.

- Investors should focus on why management is undertaking a corporate action.

- Neither bonus shares nor stock splits create wealth by themselves.

- Long-term returns depend primarily on business performance rather than corporate announcements.

Lesson 6: Buybacks, Rights Issues & QIPs – Understanding Capital Allocation Decisions

One of management’s most important responsibilities is deciding how capital should be allocated.

At different stages of its life cycle, a company may need additional capital to fund growth, reduce debt, acquire businesses, or strengthen operations. At other times, the company may generate more cash than it can efficiently use.

These situations often lead to corporate actions such as:

- Buybacks

- Rights Issues

- Qualified Institutional Placements (QIPs)

- Preferential Allotments

Understanding these actions helps investors answer an important question:

Is management creating value for shareholders, or merely changing the ownership structure?

The answer often depends on why the action is being undertaken.

Buybacks: Returning Capital to Shareholders

A buyback occurs when a company repurchases its own shares from existing shareholders.

Instead of using excess cash for expansion or acquisitions, management chooses to return capital by reducing the number of shares outstanding.

Example

Suppose a company has:

100 crore shares outstanding

The company buys back:

10 crore shares

After completion:

90 crore shares remain outstanding.

Existing shareholders now own a larger percentage of the company without purchasing additional shares.

Why Do Companies Conduct Buybacks?

Several reasons may exist.

Excess Cash

The company generates more cash than it currently needs.

Limited Expansion Opportunities

Management may believe reinvesting capital will generate lower returns than returning it to shareholders.

Undervaluation

Management may believe the stock is trading below its intrinsic value.

Improving Financial Metrics

Reducing the share count can increase earnings per share (EPS).

When Is a Buyback Positive?

Buybacks are often viewed favorably when:

✓ The company generates strong cash flows.

✓ Debt levels remain manageable.

✓ The stock appears reasonably valued.

✓ The buyback is funded through surplus cash.

Example

A mature technology company with substantial cash reserves may choose a buyback because future investment opportunities are limited relative to available cash.

In this situation, returning capital can be a rational decision.

When Should Investors Be Careful?

Not every buyback is shareholder-friendly.

Potential Warning Signs

⚠ Borrowing money to fund buybacks.

⚠ Conducting buybacks while business fundamentals weaken.

⚠ Small symbolic buybacks that have little economic impact.

⚠ Management focusing on short-term stock price support.

The key question is:

Is the buyback improving shareholder value or simply improving appearances?

Rights Issues: Raising Capital from Existing Shareholders

A rights issue allows existing shareholders to purchase additional shares before they are offered to the public.

These shares are usually offered at a discount to the current market price.

Example

Suppose an investor owns:

100 shares

The company announces:

1 Rights Share for every 5 shares held.

The investor becomes eligible to purchase:

20 additional shares.

Why Do Companies Use Rights Issues?

Rights issues are often used when companies need capital but want existing shareholders to receive priority.

Common reasons include:

- Expansion projects

- Debt reduction

- Working capital requirements

- Acquisitions

Why Rights Issues Deserve Careful Analysis

The announcement itself is neither good nor bad.

Investors must understand why the money is needed.

Example 1: Positive Scenario

A profitable company raises funds to build a new manufacturing facility expected to increase future earnings.

This may create long-term value.

Example 2: Concerning Scenario

A heavily indebted company raises money primarily to survive financial stress.

The implications are very different.

The same corporate action can signal opportunity or risk depending on the underlying reason.

Dilution Risk

One important concept investors must understand is dilution.

Suppose shareholders choose not to participate in a rights issue.

Their ownership percentage may decline as new shares are issued.

This is why rights issues require active evaluation rather than passive observation.

Qualified Institutional Placements (QIPs)

A QIP is a mechanism through which listed companies raise capital directly from institutional investors.

Unlike a rights issue, the company does not approach all shareholders.

Instead, shares are allocated to qualified institutional participants.

Examples include:

- Mutual Funds

- Insurance Companies

- Pension Funds

- Foreign Institutional Investors

Why Do Companies Use QIPs?

QIPs offer several advantages:

- Faster execution

- Efficient capital raising

- Access to large investors

- Lower regulatory complexity compared with some alternatives

As a result, QIPs have become a popular fundraising tool for listed companies.

The Investor’s Perspective

When a company announces a QIP, investors should ask:

Why is the company raising money?

How will the funds be used?

Is the capital expected to generate attractive returns?

What level of dilution will existing shareholders face?

The quality of the capital allocation decision matters more than the fundraising method itself.

Preferential Allotments

In a preferential allotment, a company issues shares to a select group of investors rather than all shareholders.

Recipients may include:

- Promoters

- Strategic Investors

- Institutions

- Private Equity Funds

Because ownership structures can change significantly, investors should examine these transactions carefully.

Key Question

Whenever a preferential allotment occurs, ask:

Why were these investors chosen?

Understanding the answer often provides valuable insight into management’s intentions.

How Smart Investors Analyze Corporate Fundraising

Most investors focus on the announcement.

Professional investors focus on the purpose.

Whenever a company raises capital, ask:

Why is money needed?

How will it be deployed?

What return is expected on that capital?

Will shareholders benefit from the decision?

Is dilution justified?

These questions often reveal more than the corporate action itself.

Green Flags vs Red Flags

Positive Signs

✓ Capital raised for growth opportunities.

✓ Clear explanation of fund utilization.

✓ Strong return potential on new investments.

✓ Buybacks funded through surplus cash.

✓ Management with a good capital allocation track record.

Warning Signs

⚠ Frequent fundraising without visible results.

⚠ Capital raised to cover recurring operational problems.

⚠ Excessive dilution.

⚠ Buybacks funded by debt.

⚠ Poor disclosure regarding fund utilization.

The Most Important Lesson

Corporate actions involving capital raising or capital return should never be viewed in isolation.

A buyback is not automatically good.

A rights issue is not automatically bad.

A QIP is not automatically positive.

The true impact depends on why management is making the decision and whether it improves long-term shareholder value.

Successful investors learn to look beyond the announcement and focus on the underlying economics.

Key Takeaways

- Buybacks return capital by reducing the number of shares outstanding.

- Rights issues allow existing shareholders to participate in fundraising.

- QIPs raise capital directly from institutional investors.

- Preferential allotments issue shares to selected investors.

- Every corporate action should be evaluated based on its purpose and impact.

- Understanding capital allocation is more important than understanding the announcement itself.

- The best corporate actions create long-term shareholder value rather than short-term excitement.

Lesson 7: Mergers, Demergers & Corporate Restructuring – Creating Value or Destroying It?

As businesses grow, management sometimes decides that the existing structure of the company is no longer the most effective way to operate.

A company may choose to:

- Acquire another business

- Merge with a competitor

- Separate divisions into independent companies

- Sell non-core operations

- Reorganize business segments

These decisions are collectively known as corporate restructuring.

Such actions can significantly affect shareholders because they often change the future direction, growth prospects, risks, and valuation of the business.

However, investors should remember an important principle:

Not every merger creates value.

Not every demerger creates value.

Not every restructuring benefits shareholders.

The key is understanding why the change is taking place.

Mergers & Acquisitions (M&A)

A merger or acquisition occurs when one company combines with or purchases another business.

Management usually presents these transactions as opportunities to:

- Increase market share

- Expand into new markets

- Acquire technology

- Add products or services

- Improve efficiency

- Accelerate growth

In theory, combining two businesses should create a stronger company.

In practice, success depends entirely on execution.

Example

Imagine a large automobile manufacturer acquires an EV technology company.

Management may believe the acquisition will:

- Accelerate EV development

- Reduce research time

- Improve competitiveness

If integration succeeds, shareholders may benefit.

If integration fails, the acquisition may become an expensive mistake.

This is why investors should evaluate the logic behind the transaction rather than assuming every acquisition is positive.

Why Acquisitions Fail

Many acquisitions look attractive on paper but struggle in reality.

Common reasons include:

Overpaying

Management may become overly optimistic and pay too much for the target company.

Even a good business can become a poor investment if acquired at an excessive price.

Integration Problems

Combining employees, systems, cultures, and operations can be far more difficult than expected.

Unrealistic Expectations

Projected synergies sometimes fail to materialize.

Costs remain high while expected benefits never arrive.

For investors, this means that a large acquisition announcement should be analyzed carefully rather than celebrated automatically.

Demergers: Unlocking Hidden Value

A demerger occurs when a company separates one or more business divisions into independent entities.

Instead of operating under a single corporate structure, the businesses become separate companies.

Why Do Companies Demerge?

Management may choose a demerger when:

- Businesses operate in very different industries.

- One division is growing faster than another.

- Investors struggle to value the combined company.

- Management wants greater strategic focus.

Demergers are often described as attempts to unlock value that may be hidden within a larger organization.

Example

Imagine a company operating:

- A fast-growing technology business

- A slow-growing manufacturing business

Investors may value the combined entity conservatively because both businesses are bundled together.

After a demerger:

- Each business can be evaluated independently.

- Investors can choose exposure to the segment they prefer.

- Valuations may become more transparent.

This is one reason demergers sometimes create shareholder value.

Conglomerates and the Conglomerate Discount

Some companies operate across numerous unrelated industries.

Examples might include businesses involved in:

- Manufacturing

- Financial Services

- Energy

- Consumer Products

Such structures are known as conglomerates.

Investors sometimes apply a “conglomerate discount” because:

- Complexity increases.

- Capital allocation becomes difficult to evaluate.

- Business performance becomes harder to analyze.

A demerger may reduce this complexity and allow each business to receive a more appropriate valuation.

Corporate Restructuring

Not all restructuring involves mergers or demergers.

Companies may also:

- Sell non-core assets

- Shut unprofitable divisions

- Reorganize business units

- Exit declining industries

These decisions often aim to improve efficiency and focus management attention on the strongest opportunities.

Example

A company operating:

- Consumer Products

- Real Estate

- Hospitality

may decide to exit hospitality and focus entirely on consumer products.

Investors should evaluate whether the restructuring strengthens the company’s competitive position.

Who Benefits?

This is the most important question investors should ask.

Potential Beneficiaries

- Shareholders

- Promoters

- Management

- Acquiring Companies

- Target Companies

Sometimes everyone benefits.

Sometimes only certain groups benefit.

Understanding incentives is critical.

Questions Investors Should Ask

Whenever a merger, acquisition, or demerger is announced:

Why is this transaction happening?

How does it improve the business?

Is management paying a reasonable price?

Does the transaction create strategic advantages?

Who benefits most from the change?

What risks are involved?

The quality of the answers often matters more than the announcement itself.

Green Flags vs Red Flags

Positive Signs

✓ Clear strategic rationale.

✓ Strong management track record.

✓ Reasonable acquisition pricing.

✓ Improved business focus.

✓ Better capital allocation.

✓ Transparent communication.

Warning Signs

⚠ Acquisitions made primarily for size or prestige.

⚠ Excessive debt-funded transactions.

⚠ Poor disclosure.

⚠ Complicated restructuring with unclear benefits.

⚠ Repeated acquisitions without successful integration history.

⚠ Management unable to explain expected shareholder benefits.

The Most Important Lesson

Many investors react to restructuring announcements without understanding their purpose.

Successful investors take a different approach.

They ask:

Is this transaction making the business stronger?

Corporate restructuring should not be judged by headlines.

It should be judged by whether it improves long-term shareholder value.

Some of the best corporate actions in market history have unlocked enormous value.

Some of the worst have destroyed it.

Understanding the difference is one of the most valuable skills an investor can develop.

Key Takeaways

- Mergers and acquisitions aim to strengthen businesses through expansion, scale, or strategic advantages.

- Demergers separate businesses to improve focus and unlock value.

- Corporate restructuring can improve efficiency, capital allocation, and strategic direction.

- Not all restructuring creates value; execution matters.

- Investors should focus on the purpose, economics, and incentives behind every transaction.

- The key question is not what management announced, but whether the decision improves long-term shareholder value.

Lesson 8: Promoters, Insider Activity & Corporate Signals – Reading Management’s Actions

Every listed company has shareholders, but not all shareholders are equal.

Some own the business.

Some manage the business.

Some invest in the business.

Among the most important groups are:

- Promoters

- Founders

- Senior Management

- Directors

- Key Employees

Because these individuals are closest to the business, investors often monitor their actions for clues about management confidence, capital allocation, and potential risks.

However, promoter and insider activity should never be interpreted in isolation.

A single transaction rarely tells the full story.

The goal is not to blindly follow insiders.

The goal is to understand the signal behind their actions.

Who Are Promoters?

Promoters are the individuals, families, or entities responsible for establishing and controlling a company.

In many Indian businesses, promoters remain significant shareholders even after listing.

Because they often have substantial personal wealth tied to the company, their decisions can have a major impact on shareholder outcomes.

This is why investors pay close attention to promoter behavior.

Promoter Shareholding

One of the simplest indicators investors track is promoter ownership.

Questions worth asking include:

- How much of the company do promoters own?

- Has ownership increased or decreased?

- Has the trend remained stable over time?

Why It Matters

Promoters with meaningful ownership often have strong alignment with shareholders because both benefit from long-term value creation.

However, high ownership alone is not enough.

Governance and capital allocation still matter.

Promoter Buying

When promoters purchase additional shares from the market, investors often interpret it as a positive signal.

Why?

Because management is voluntarily increasing exposure to its own business.

Example

Suppose a promoter already owns 50% of a company and purchases additional shares using personal funds.

This may indicate:

- Confidence in future prospects

- Belief that the stock is undervalued

- Long-term commitment to the business

However, investors should evaluate the scale of the purchase.

A small purchase may generate headlines but have little economic significance.

Always focus on materiality rather than publicity.

Promoter Selling

Promoter selling often attracts negative attention.

Many investors immediately assume:

“The promoter is selling, something must be wrong.”

Reality is usually more complex.

Promoters may sell shares for many reasons:

- Diversification

- Tax planning

- Estate planning

- Family settlements

- Funding other ventures

- Philanthropic activities

Example

A promoter owning 75% of a company may reduce ownership to 72%.

This does not automatically indicate a problem.

However, repeated or substantial reductions without clear explanation deserve closer attention.

The pattern matters more than the individual transaction.

Insider Buying and Selling

Insiders include:

- Directors

- Senior executives

- Key management personnel

Because insiders often possess deep knowledge of the business, their trading activity receives significant attention.

Insider Buying

Generally viewed as a constructive signal because management is increasing personal exposure.

Insider Selling

Requires context.

Like promoters, insiders may sell for personal financial reasons unrelated to business performance.

Investors should focus on:

- Frequency

- Size

- Consistency

- Timing

rather than reacting to isolated transactions.

Promoter Pledge: One of the Most Important Signals

A promoter pledge occurs when promoters use their shares as collateral to secure loans.

This is one of the most important corporate signals investors should monitor.

Why Promoters Pledge Shares

Promoters may require capital for:

- Business expansion

- Personal investments

- Group companies

- Debt obligations

To obtain financing, they pledge shares as collateral.

Why Investors Should Care

If the share price falls significantly, lenders may demand additional collateral or sell pledged shares.

This can create:

- Selling pressure

- Increased volatility

- Governance concerns

Example

Suppose:

Promoter Holding = 60%

Promoter Pledge = 45%

A large portion of promoter ownership is now linked to external financing arrangements.

This deserves careful analysis.

Is Every Pledge Bad?

No.

A temporary and moderate pledge for productive business purposes may not be problematic.

However, investors should become cautious when:

- Pledge levels remain high.

- Pledges continue increasing.

- Financial stress appears elsewhere in the business.

The trend often matters more than the headline number.

Reading Management Signals

Many investors focus only on what management says.

Experienced investors often pay greater attention to what management does.

Examples include:

Positive Signals

- Increasing ownership

- Reducing debt

- Eliminating promoter pledges

- Improving disclosures

- Consistent capital allocation decisions

Warning Signals

- Persistent ownership reduction

- Increasing pledges

- Frequent equity dilution

- Poor transparency

- Repeated fundraising without results

Actions often reveal more than words.

Corporate Governance Matters

Even a strong business can become a poor investment if governance standards are weak.

Investors should evaluate:

- Transparency

- Shareholder treatment

- Related-party transactions

- Capital allocation decisions

- Disclosure quality

Good governance helps build long-term trust between management and shareholders.

Poor governance can destroy value regardless of business quality.

Green Flags vs Red Flags

Positive Signs

✓ Stable or increasing promoter ownership.

✓ Low or declining promoter pledges.

✓ Meaningful insider buying.

✓ Transparent communication.

✓ Shareholder-friendly capital allocation.

✓ Strong governance practices.

Warning Signs

⚠ Rising promoter pledges.

⚠ Frequent unexplained selling.

⚠ Repeated dilution.

⚠ Weak disclosures.

⚠ Governance controversies.

⚠ Management actions that consistently favor insiders over minority shareholders.

The Most Important Lesson

Promoters and insiders often know the business better than anyone else.

Their actions can provide valuable clues.

However, no single transaction should be viewed as a buy or sell signal.

The objective is to identify patterns.

Successful investors study:

- Ownership trends

- Pledge levels

- Insider activity

- Governance quality

and then combine those observations with business analysis and valuation.

The smartest approach is neither blind trust nor automatic suspicion.

It is careful observation supported by independent thinking.

Key Takeaways

- Promoters and insiders can provide valuable signals through their actions.

- Promoter buying and insider buying may indicate confidence, but context matters.

- Promoter selling is not automatically negative and should be evaluated carefully.

- Promoter pledges are an important risk indicator that investors should monitor closely.

- Governance quality often has a major influence on long-term shareholder outcomes.

- Investors should focus on trends and patterns rather than isolated transactions.

- Management actions often reveal more than management statements.

Conclusion

Understanding IPOs and corporate actions helps investors look beyond stock prices and better understand the businesses they invest in.

IPOs reveal why companies enter public markets, how capital is raised, and how investors can evaluate new opportunities. Corporate actions reveal how management allocates capital, treats shareholders, restructures businesses, and makes decisions that influence long-term value creation.

The most important lesson is that every IPO and every corporate action has a purpose. Successful investors do not focus only on the event itself—they focus on the reason behind it, the incentives involved, and its impact on future shareholder value.

By understanding both, investors can make more informed decisions and develop a deeper understanding of how companies interact with capital markets throughout their life cycle.

External Resources

For the latest IPO information, corporate announcements, corporate actions, shareholding disclosures, and regulatory filings, investors can refer to:

- National Stock Exchange (NSE)

- Bombay Stock Exchange (BSE)

These exchanges provide official information regarding IPOs, dividends, bonus issues, stock splits, buybacks, rights issues, mergers, shareholding patterns, and other important corporate developments.