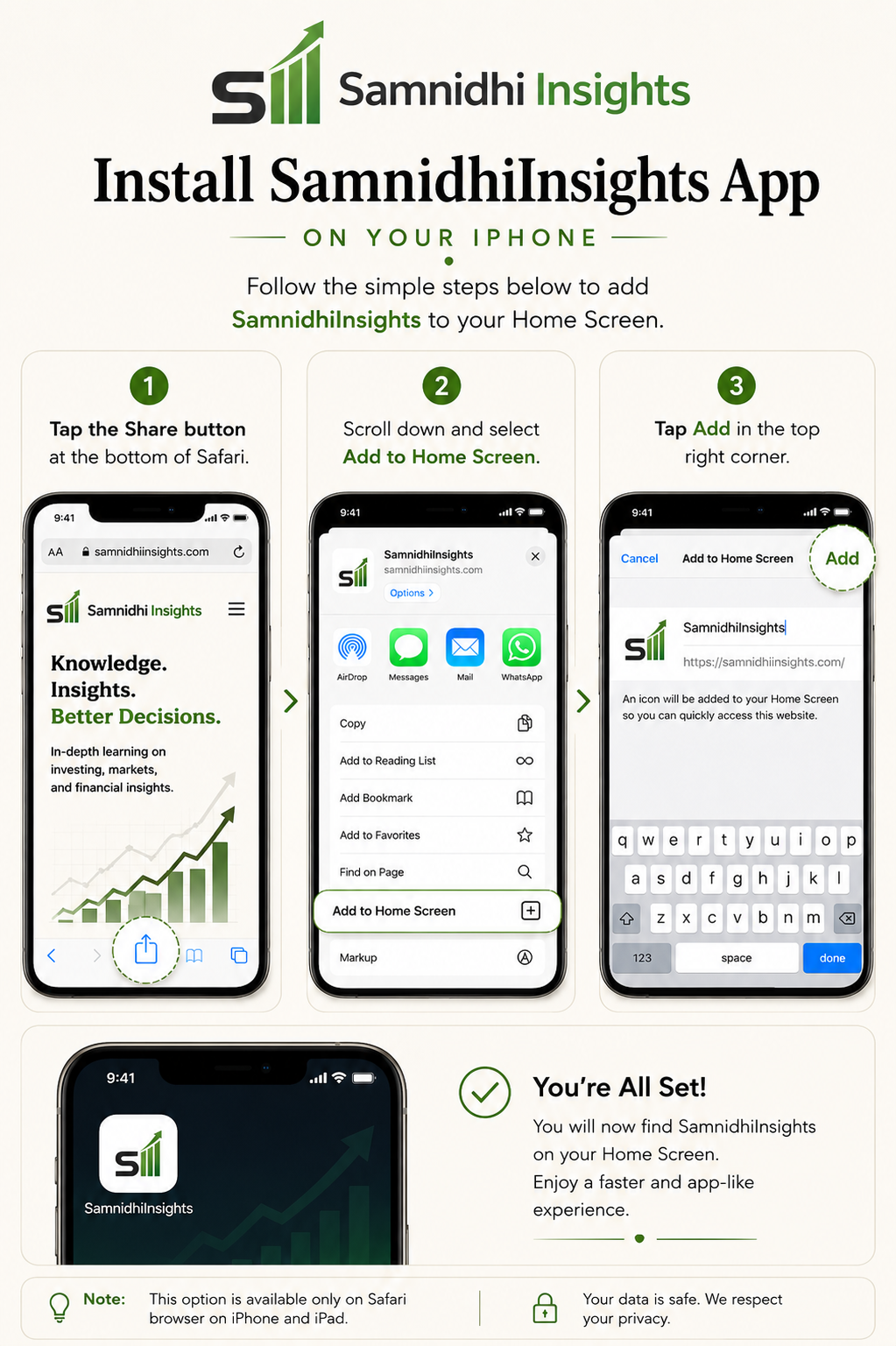

Getting Started with Investing in India

Starting your investing journey can feel overwhelming. Terms such as PAN, KYC, Demat accounts, brokers, mutual funds, and stock markets often create confusion for first-time investors.

The purpose of this section is to simplify the process and help you build a strong investing foundation before putting your money to work.

Whether you’re opening your first Demat account, completing KYC verification, understanding how the Indian investing ecosystem works, or preparing to make your first investment, these guides are designed to provide clear, practical, and beginner-friendly explanations.

The goal is not simply to start investing quickly, but to start investing with knowledge, confidence, and the right foundation for long-term success.

Lesson 1: Why Getting Started Matters & How Investing Works in India

Building the Foundation Before Building Wealth

Why This Lesson Matters

Most investing mistakes do not happen after years of experience.

They happen at the very beginning.

Many new investors spend hours searching for:

- The best stock

- The next multibagger

- The hottest sector

- The highest return opportunity

But spend very little time understanding how investing actually works.

As a result, they often:

- Open accounts without understanding their purpose

- Choose brokers based on advertisements

- Follow social media recommendations blindly

- Confuse trading with investing

- Focus on returns without understanding risk

- Enter the market with unrealistic expectations

These mistakes may appear small, but they can create confusion, poor decisions, and unnecessary losses later.

Successful investing rarely begins with finding the perfect stock.

It begins with understanding the system you are participating in.

Just as a person should understand traffic rules before driving a car, an investor should understand how the investing ecosystem works before risking capital.

The objective of this lesson is to build that foundation.

┌─────────────┐

│ 📘 START │

└─────────────┘

┌─────────────┐

│ 💻 EXECUTE │

└─────────────┘

┌─────────────┐

│ 🧮 PLAN │

└─────────────┘

┌─────────────┐

│ 📊 ANALYZE │

└─────────────┘

┌─────────────┐

│ 📚 LEARN │

└─────────────┘

┌─────────────┐

│ 🤖 AI & TECH│

└─────────────┘

🎯 Better Decisions

What Investing Really Means

Before discussing brokers, Demat accounts, or stock exchanges, it is important to understand what investing actually is.

When people hear the word “investing,” they often imagine buying a stock and watching it rise in value.

In reality, investing is much deeper than that.

Investing means allocating money today with the expectation of creating greater value in the future.

That future value may come from:

- Business growth

- Dividends

- Interest income

- Economic expansion

- Asset appreciation

At its core, investing is the process of putting money to work rather than leaving it idle.

For example:

Suppose two people each have ₹10,000.

Person A spends the entire amount on things that lose value over time.

Person B invests the amount into productive assets.

Over the next decade, the outcomes may be dramatically different.

The difference is not income.

The difference is how capital was allocated.

Investing is ultimately about ownership.

When you buy shares of a company, you become a partial owner of that business.

Understanding this simple idea changes how you view markets.

You are not merely buying a ticker symbol.

You are buying a stake in a real business.

Why Many Beginners Feel Confused

One reason investing appears complicated is that most beginners only see the front end of the process.

They open an app.

Search for a stock.

Press Buy.

And the transaction appears complete.

Behind the scenes, however, several organizations work together to make that simple action possible.

Because these systems operate automatically, many investors never understand what happens after they press the Buy button.

Understanding this process removes a great deal of confusion and makes the investing journey much easier.

The Indian Investing Ecosystem

Think of investing as a team effort involving multiple participants.

Each participant performs a specific role.

Together, they create a secure and efficient system for buying, selling, and holding investments.

Let’s meet the key participants.

You: The Investor

Every investment journey begins with you.

You provide the capital.

You decide where that capital will be invested.

You determine:

- Your goals

- Your risk tolerance

- Your time horizon

- Your investment decisions

Everyone else in the system provides infrastructure.

You provide the decision.

This distinction is important because responsibility always remains with the investor.

The Broker: Your Gateway to the Market

Imagine you want to purchase shares of a company.

You cannot directly walk into the National Stock Exchange and place an order yourself.

Instead, you need an intermediary.

That intermediary is called a broker.

A broker provides the platform through which investors buy and sell securities.

Examples include:

- Zerodha

- Groww

- Upstox

- Angel One

- ICICI Direct

The broker acts as a bridge between investors and stock exchanges.

Without a broker, participation in the stock market would be difficult for most retail investors.

Think of the broker as the doorway that connects you to the market.

The Stock Exchange: Where Buyers and Sellers Meet

Once you place an order, it is routed to a stock exchange.

India’s two primary stock exchanges are:

National Stock Exchange (NSE)

Bombay Stock Exchange (BSE)

These exchanges provide the marketplace where buyers and sellers interact.

Imagine a giant digital marketplace where millions of participants place orders every day.

The exchange matches these orders and facilitates transactions.

Importantly, exchanges do not provide investment advice.

Their role is to ensure that transactions occur fairly, efficiently, and transparently.

The Depository: The Invisible Vault

Suppose you successfully purchase shares.

Where do those shares go?

Many beginners assume the broker holds them.

That is not entirely correct.

The actual ownership records are maintained by depositories.

India has two major depositories:

NSDL

National Securities Depository Limited

CDSL

Central Depository Services Limited

These institutions maintain electronic records of ownership.

Think of them as highly secure digital vaults that keep track of who owns what.

Without depositories, modern investing would be far more complicated.

The Demat Account: Your Digital Investment Locker

The shares you purchase are credited to your Demat account.

The word “Demat” stands for Dematerialized.

Years ago, investors received physical share certificates.

These certificates could:

- Be lost

- Be damaged

- Be stolen

- Be forged

Demat accounts solved these problems by converting ownership records into electronic form.

A useful way to think about a Demat account is this:

A bank account stores money.

A Demat account stores investments.

The Demat account itself does not generate returns.

Its purpose is safekeeping.

Your Bank Account: The Source of Capital

Every investment transaction ultimately involves money.

When you buy investments:

Money leaves your bank account.

When you sell investments:

Money returns to your bank account.

Your bank account acts as the financial foundation of your investing activities.

This is why account verification and proper banking setup become important later in the process.

What Actually Happens When You Buy a Stock?

Let’s bring everything together.

Imagine you decide to purchase shares worth ₹10,000.

Here’s what happens behind the scenes.

Step 1

You place a buy order through your broker.

Step 2

The broker sends the order to the stock exchange.

Step 3

The exchange matches your order with a seller.

Step 4

The money is debited from your linked bank account.

Step 5

Ownership records are updated through the depository.

Step 6

The shares are credited to your Demat account.

The entire process usually happens so smoothly that investors rarely notice the complexity behind it.

Yet understanding this flow provides clarity that many beginners lack.

The Simplified Investing Flow

Share Flow

Investor

↓

Broker

↓

Stock Exchange

↓

Depository

↓

Demat Account

Money Flow

Bank Account

↓

Investment Purchase

↓

Ownership of Securities

Every investment transaction follows this basic structure.

Understanding it eliminates much of the confusion beginners experience when opening accounts or making their first investment.

Why This Knowledge Matters

Some investors may wonder:

“Do I really need to understand all of this?”

The answer is yes.

Not because you need to memorize every institution.

But because understanding the ecosystem helps you:

- Open accounts with confidence

- Avoid common misconceptions

- Understand where your investments are held

- Understand who performs which role

- Make better decisions as an investor

Confidence often comes from understanding.

And understanding begins with knowing how the system works.

Key Takeaway

Investing is not simply about buying stocks.

It is about participating in a structured ecosystem designed to help investors own financial assets safely and efficiently.

Before selecting investments, every investor should understand the roles played by:

- Brokers

- Stock exchanges

- Depositories

- Demat accounts

- Bank accounts

Together, these institutions form the foundation of the Indian investing system.

In the next lesson, we will move from understanding the ecosystem to building your personal investing foundation by preparing the documents, verification requirements, and infrastructure needed to begin your investing journey.

Lesson 2: Building Your Investing Foundation

Preparing the Infrastructure Behind Every Successful Investor

Why This Lesson Matters

When people imagine investing, they think about:

- Stocks

- Mutual funds

- Returns

- Wealth creation

Almost nobody gets excited about:

- PAN cards

- KYC verification

- Aadhaar linking

- Bank account checks

Yet these are often the first obstacles investors encounter.

Many beginners spend more time searching for stock tips than preparing the infrastructure required to invest properly.

As a result, they face:

- Account opening delays

- Verification failures

- Transaction issues

- Withdrawal problems

- Regulatory restrictions

None of these problems are difficult to solve.

But they become frustrating when discovered at the wrong time.

Imagine spending weeks researching an investment opportunity only to discover that your account cannot be activated because of a PAN mismatch.

The market is not the problem.

Preparation is.

Before building a portfolio, every investor should build a strong foundation.

This lesson explains how.

Think Like a Builder

Imagine constructing a house.

Most people focus on what is visible:

- Walls

- Windows

- Paint

- Furniture

The most important work, however, happens before any of that appears.

The foundation is built first.

If the foundation is weak, everything above it becomes vulnerable.

Investing works the same way.

Stocks and mutual funds are the visible part.

Identity verification, banking infrastructure, and regulatory compliance form the foundation.

The stronger the foundation, the smoother the investing journey.

Step 1: Your PAN Card — The Backbone of Your Investing Identity

If there is one document that sits at the center of the Indian investing ecosystem, it is your PAN card.

Almost every major investing activity is linked to PAN.

It is used for:

- Account opening

- KYC verification

- Tax reporting

- Investment records

- Regulatory compliance

Think of PAN as your financial identity within the investing system.

Without it, most investing activities cannot proceed.

Why PAN Issues Create Problems

Many investors assume that possessing a PAN card is enough.

In reality, several common issues create complications:

- PAN not linked to Aadhaar

- Incorrect name spelling

- Different initials across documents

- Incorrect date of birth

- Outdated records

These may appear minor.

To financial systems, they are not.

A small mismatch can trigger verification failures and delays.

Practical Example

Imagine the following situation:

PAN Name:

Rajesh Kumar Sharma

Bank Account Name:

Rajesh K Sharma

Aadhaar Name:

Rajesh Sharma

To a human, these appear similar.

To a verification system, they may not.

This can create unnecessary friction during account opening.

A few minutes spent reviewing your records can save days of frustration later.

Before Moving Forward

Confirm that:

✔ PAN is active

✔ PAN is linked to Aadhaar

✔ Name is consistent across documents

✔ Date of birth is correct

✔ Mobile number is current

This is the first layer of your investing foundation.

Step 2: Aadhaar & Mobile Verification

Most modern investing processes are completed digitally.

Verification often depends on:

- Aadhaar authentication

- OTP verification

- Mobile-linked services

This makes your mobile number more important than many investors realize.

Why This Matters

Imagine opening an account.

Everything progresses smoothly until the final verification stage.

The OTP is sent to a mobile number that you no longer use.

Now the process stops.

Not because of investing knowledge.

Not because of regulations.

Simply because your records were not updated.

Investor Mindset

Treat your Aadhaar-linked mobile number like a key.

Many important financial activities depend on it.

Maintaining accurate records today prevents unnecessary problems tomorrow.

Step 3: Your Bank Account — The Engine Behind Every Investment

Every investment transaction eventually flows through a bank account.

When you buy:

Money leaves your bank account.

When you sell:

Money returns to your bank account.

When dividends are paid:

They are credited to your bank account.

When withdrawals occur:

They move through your bank account.

In many ways, your bank account acts as the financial engine behind your investing activities.

Common Beginner Mistakes

Some investors attempt to use:

- Dormant accounts

- Rarely used accounts

- Accounts with outdated details

Others discover too late that:

- Net banking is inactive

- UPI verification is failing

- Contact details are outdated

These issues often surface during critical moments.

A Better Approach

Before investing, ensure:

✔ Account is active

✔ Online banking is working

✔ UPI is functioning

✔ Name matches PAN records

✔ Mobile number is updated

Think of this as a pre-flight check before takeoff.

Step 4: Understanding KYC

KYC stands for:

Know Your Customer

Most investors view KYC as paperwork.

In reality, KYC exists because financial systems require trust and accountability.

Why KYC Exists

Imagine a financial system where anyone could open accounts anonymously.

Fraud would become significantly easier.

Identity theft would increase.

Regulatory oversight would weaken.

Investor protection would suffer.

KYC helps prevent these problems.

What KYC Achieves

KYC helps:

- Verify identity

- Reduce fraud

- Improve transparency

- Protect investors

- Support regulatory compliance

In short:

KYC helps create a safer investing ecosystem for everyone.

Why Beginners Often Dislike KYC

The answer is simple.

KYC does not feel productive.

Investors want to:

- Open accounts

- Buy investments

- Start earning returns

KYC feels like a delay.

However, the reality is different.

A properly completed KYC process often makes future investing significantly smoother.

Think of it as a one-time inconvenience that prevents recurring problems.

Full KYC vs Basic Verification

Whenever possible, complete the most comprehensive verification available.

Many investors choose simplified options because they appear faster.

Later they discover:

- Additional restrictions

- Upgrade requirements

- Extra verification requests

Completing the process correctly from the beginning is usually the better choice.

The Hidden Cost of Poor Preparation

Most investing mistakes are visible.

Buying the wrong stock.

Selling too early.

Taking excessive risk.

Infrastructure mistakes are different.

They are invisible until something breaks.

Example

Suppose you need to:

- Withdraw funds quickly

- Update account details

- Complete tax documentation

- Activate a new investment account

A small documentation mismatch can suddenly become a major inconvenience.

The objective of preparation is not excitement.

The objective is reliability.

Strong foundations are rarely noticed.

Weak foundations eventually are.

Your Investing Foundation Checklist

Before opening a broker account, verify the following:

Identity Readiness

✔ PAN active

✔ PAN linked to Aadhaar

✔ Name matches across documents

✔ Date of birth consistent

✔ Mobile number updated

Banking Readiness

✔ Active bank account

✔ Net banking enabled

✔ UPI functioning

✔ Contact details updated

✔ Name matches official records

Verification Readiness

✔ KYC completed

✔ Documents accessible

✔ Email and mobile verification working

Why This Foundation Matters

Many investors believe investing begins when they buy their first stock.

In reality, investing begins much earlier.

It begins with preparation.

The smoother your infrastructure, the less time you spend solving administrative problems and the more time you spend focusing on what actually matters:

- Learning

- Research

- Decision-making

- Long-term wealth creation

Professional investors understand this.

Strong systems create smoother outcomes.

Key Takeaway

Before selecting investments, every investor should build a reliable foundation.

PAN verification, Aadhaar linking, banking readiness, and KYC completion may not feel exciting, but they form the infrastructure that supports every future investment decision.

Great investing journeys rarely begin with a stock tip.

They begin with preparation.

In the next lesson, we will explore Demat accounts, trading accounts, broker selection, and how to choose the right investing platform for your needs.

Lesson 3: Demat Accounts & Choosing the Right Broker

Understanding Where Your Investments Are Stored and How to Access the Market

Why This Lesson Matters

After completing your PAN verification, KYC, and banking setup, the next step is opening an investment account.

This is usually the stage where beginners encounter terms such as:

- Demat Account

- Trading Account

- Broker

- Depository Participant

- Brokerage Charges

For many new investors, these terms sound complicated.

The good news is that the underlying concepts are actually quite simple once you understand their purpose.

The challenge is that many investors open accounts without understanding what each component does.

As a result, they often become confused about:

- Where their investments are stored

- Who owns their investments

- What the broker actually does

- Why charges exist

- How transactions are processed

The purpose of this lesson is to eliminate that confusion and help you choose the right broker based on your needs rather than advertisements or popularity.

A Common Beginner Misconception

Let’s start with one of the most common misunderstandings.

Ask a new investor:

“Where are your shares stored?”

Many will answer:

“With my broker.”

This answer is only partially correct.

Your broker helps you buy and sell investments.

Your broker does not ultimately own or hold your investments.

This distinction is extremely important.

To understand why, let’s first understand the role of a Demat account.

What Is a Demat Account?

Demat stands for:

Dematerialized Account

The term may sound technical, but the idea is straightforward.

A Demat account is a digital account that holds your investments electronically.

Think of it as a locker for financial assets.

Just as a bank account stores money, a Demat account stores investments such as:

- Shares

- Exchange-Traded Funds (ETFs)

- Bonds

- Government Securities

- REITs

- InvITs

The account itself does not generate returns.

Its purpose is safekeeping.

Why Demat Accounts Were Created

To appreciate the importance of Demat accounts, imagine investing thirty years ago.

When investors purchased shares, they received physical share certificates.

These certificates represented ownership.

Unfortunately, physical certificates created many problems.

They could:

- Be lost

- Be stolen

- Be damaged

- Be forged

- Take weeks to transfer

Imagine owning shares worth several lakhs and discovering that the certificates had been misplaced.

The process of proving ownership could become extremely difficult.

Demat accounts solved these problems by replacing paper certificates with electronic ownership records.

Today, ownership can be tracked securely and efficiently.

This was one of the most important developments in the modernization of Indian financial markets.

Who Actually Holds Your Investments?

Many investors assume brokers store their shares.

This is not entirely accurate.

The actual ownership records are maintained through India’s depositories:

NSDL

National Securities Depository Limited

CDSL

Central Depository Services Limited

These organizations act as the backbone of the Demat system.

Think of them as highly secure digital vaults.

They maintain records of ownership for millions of investors.

Your broker acts as an intermediary.

The depository maintains the ownership records.

This separation adds an important layer of security.

Understanding the Trading Account

One of the biggest sources of confusion for beginners is the difference between a Demat account and a Trading account.

Let’s simplify it.

The Demat Account

Purpose:

Stores investments

Think:

Storage

The Trading Account

Purpose:

Buys and sells investments

Think:

Transaction engine

A Simple Analogy

Imagine purchasing a book online.

The shopping website helps you make the purchase.

Your bookshelf stores the book after delivery.

The shopping website and the bookshelf perform different functions.

Similarly:

Trading Account = Purchase and Sale

Demat Account = Storage

Both are necessary.

But they perform different roles.

The Three-Account System

Most investing transactions involve three connected accounts.

Bank Account

Stores money.

Trading Account

Facilitates buying and selling.

Demat Account

Stores investments.

What Happens When You Buy a Stock?

Suppose you purchase shares worth ₹20,000.

Step 1

Money leaves your bank account.

↓

Step 2

The trading account places the order.

↓

Step 3

The stock exchange matches the order.

↓

Step 4

Ownership is updated through the depository.

↓

Step 5

Shares appear in your Demat account.

Understanding this flow eliminates much of the confusion surrounding investing accounts.

Who Is a Broker?

A broker is simply the organization that provides access to financial markets.

Without a broker, retail investors cannot directly place orders on stock exchanges.

A broker provides:

- Market access

- Trading platforms

- Account services

- Transaction processing

- Customer support

Think of the broker as the bridge between you and the market.

Types of Brokers in India

Broadly speaking, brokers fall into two categories.

Discount Brokers

Examples:

- Zerodha

- Groww

- Upstox

These brokers focus on:

- Low costs

- Simple platforms

- Self-directed investing

Best For

Investors who:

- Conduct their own research

- Prefer lower charges

- Want a straightforward experience

Full-Service Brokers

Examples:

- ICICI Direct

- HDFC Securities

- Kotak Securities

These brokers typically offer:

- Research reports

- Advisory support

- Relationship managers

- Additional services

Best For

Investors who prefer:

- Additional guidance

- Integrated banking relationships

- More comprehensive service offerings

Choosing the Right Broker

One of the most common beginner questions is:

“Which is the best broker?”

The better question is:

“Which broker is best for me?”

The answer depends on your investing style.

Investor Type 1: The Long-Term Investor

Typically:

- Invests monthly

- Buys quality businesses

- Holds investments for years

Priority:

- Simplicity

- Reliability

- Low cost

Investor Type 2: The Research-Oriented Investor

Typically:

- Studies companies extensively

- Tracks financial data

- Uses screening tools

Priority:

- Research capabilities

- Platform features

- Data availability

Investor Type 3: The Active Trader

Typically:

- Places frequent trades

- Uses technical analysis

- Requires speed

Priority:

- Execution quality

- Trading tools

- Platform responsiveness

Different investors may legitimately choose different brokers.

There is no universal answer.

Understanding Brokerage Charges

Many beginners obsess over brokerage charges.

Charges matter.

But they should be understood in context.

Imagine two investors.

Investor A saves ₹500 annually in brokerage but repeatedly makes poor investment decisions.

Investor B pays slightly higher charges but follows a disciplined long-term strategy.

Which investor is likely to build more wealth?

The answer is obvious.

Cost matters.

Decision quality matters more.

What Charges Should You Review?

Before selecting a broker, review:

- Account opening charges

- Annual maintenance charges (AMC)

- Brokerage fees

- Platform charges

- Other transaction-related costs

The goal is not necessarily to find the cheapest option.

The goal is to find value.

One Broker or Multiple Brokers?

Many beginners ask whether they should maintain multiple broker accounts.

For most new investors:

One well-chosen broker is sufficient.

Multiple accounts often create:

- Additional complexity

- More paperwork

- Portfolio fragmentation

As experience grows, some investors choose additional accounts for specific purposes.

At the beginning, simplicity is usually the better strategy.

A Practical Broker Selection Checklist

Before opening an account, ask:

Is the platform easy to use?

Does it support my investing style?

Are charges reasonable?

Is customer support reliable?

Do I understand all major fees?

Will I still be comfortable using this platform five years from now?

If the answer to these questions is yes, the broker is probably worth considering.

Key Takeaway

A Demat account is not an investment.

It is the secure digital locker that stores your investments.

A trading account allows you to buy and sell.

A broker provides access to the market.

A depository maintains ownership records.

Understanding these roles removes much of the confusion that new investors experience.

Choosing the right broker is not about selecting the most popular platform.

It is about selecting the platform that best aligns with your investing needs, goals, and style.

In the next lesson, we will discuss one of the most important subjects in investing: risk. Before making your first investment, it is essential to understand not only how money can grow, but also what can cause it to decline.

Lesson 4: Understanding Risk & Making Your First Investment

Why Successful Investors Think About Risk Before Returns. Ask a new investor why they want to invest, and you’ll often hear answers such as:

- To grow wealth

- To beat inflation

- To achieve financial freedom

- To earn better returns

All of these are valid goals.

However, there is one word missing from most beginner conversations:

Risk.

Many investors spend weeks researching potential returns while spending very little time understanding potential risks.

This is one of the biggest mistakes beginners make.

Because investing is not simply about making money.

It is about managing uncertainty.

Every investment opportunity comes with a trade-off.

The possibility of reward exists because risk exists.

Understanding this relationship is one of the most important lessons any investor can learn.

The Biggest Myth About Investing

One of the most common misconceptions is:

“Good investments always go up.”

Reality is very different.

Even excellent businesses experience:

- Temporary declines

- Economic slowdowns

- Market corrections

- Industry disruptions

- Unexpected challenges

Consider some of the world’s most successful companies.

Many have experienced periods where their stock prices declined significantly despite remaining strong businesses.

Price volatility is a normal part of investing.

The problem is that many beginners encounter volatility for the first time after investing.

By then, emotions often take control.

Understanding risk beforehand creates better decisions later.

What Risk Actually Means

Most beginners define risk as:

“Losing money.”

While technically true, this definition is incomplete.

A more useful definition is:

Risk is the possibility that reality turns out differently than expected.

This can happen in many ways.

A company may grow slower than anticipated.

An industry may face unexpected challenges.

Economic conditions may deteriorate.

Investor sentiment may change.

Markets constantly remind us that the future is uncertain.

Risk is not something that can be eliminated.

It can only be understood and managed.

The Different Types of Risk Every Investor Should Understand

Not all risks are the same.

Some are visible.

Others remain hidden until problems appear.

Let’s examine the most important ones.

Market Risk

Market risk affects almost everyone.

Even strong companies can decline when overall markets become fearful.

Example

Imagine investing in a fundamentally strong company.

A global recession occurs.

Investors become nervous.

Stock markets fall broadly.

Your company may decline alongside the market despite nothing changing in the business itself.

This is market risk.

The business may remain healthy.

The market environment changes.

Important Lesson

A falling stock price does not automatically mean a failing business.

Learning this distinction can save investors from many emotional decisions.

Business Risk

Business risk comes from the company itself.

Every company faces challenges such as:

- Competition

- Changing customer preferences

- Rising costs

- Regulatory changes

- Poor management decisions

Example

Imagine two smartphone manufacturers.

One continues innovating.

The other falls behind competitors.

Over time, the weaker business loses customers and profitability.

The risk came from the business, not the market.

This is why understanding a company’s fundamentals matters.

Inflation Risk

Inflation is one of the most overlooked risks.

Many people believe keeping money in a savings account is completely safe.

The reality is more complicated.

Example

Suppose inflation averages 6% annually.

Your money grows at 3%.

Although the account balance increases, purchasing power declines.

In simple terms:

Your money is growing.

But not fast enough.

Over long periods, inflation quietly erodes wealth.

One reason people invest is to protect against this risk.

Behavioural Risk

This is the risk most investors underestimate.

Markets do not usually destroy portfolios.

Investor behaviour often does.

Example

Consider two investors.

Investor A:

- Buys quality investments

- Remains disciplined

- Follows a long-term plan

Investor B:

- Chases trends

- Buys during excitement

- Sells during fear

- Constantly changes strategy

Both may have access to the same investments.

Yet their outcomes can be dramatically different.

The difference is behaviour.

Behavioural risk is often more dangerous than market risk.

Why Beginners Focus Too Much on Returns

Human nature naturally attracts us to success stories.

We enjoy hearing about:

- Multibaggers

- Market winners

- Extraordinary gains

We rarely hear about:

- Poor decisions

- Risk management

- Capital preservation

As a result, many beginners ask:

“How much can I make?”

before asking:

“What can I lose?”

Professional investors reverse the order.

They focus on protecting capital first.

Growth comes second.

Your First Investment Is Not About Making Money

This may sound surprising.

But your first investment should primarily be viewed as an educational investment.

The objective is not maximum profit.

The objective is experience.

What Should Your First Investment Teach You?

How markets move.

How emotions affect decisions.

How portfolio statements work.

How gains and losses feel.

How patience develops.

How investing differs from theory.

These lessons are difficult to learn without actual participation.

How Much Should You Invest Initially?

One of the most common beginner questions is:

“How much money should I start with?”

The answer depends on your circumstances.

However, a useful principle is:

Start small enough that mistakes will not be financially painful.

The early stage of investing is a learning phase.

Mistakes are almost inevitable.

The goal is to ensure those mistakes become lessons rather than disasters.

Example

Suppose someone has ₹1,00,000 available for investing.

A beginner may feel tempted to invest everything immediately.

A more thoughtful approach might involve:

- Starting gradually

- Learning through experience

- Building confidence

- Improving decision-making over time

Investing is a marathon.

There is rarely a need to rush.

Making Your First Investment: A Simple Roadmap

Once your account is ready and you understand basic risks, the process becomes much easier.

Step 1

Define your objective.

Why are you investing?

Examples:

- Retirement

- Wealth creation

- Financial independence

- Children’s education

Goals influence decisions.

Step 2

Understand what you are investing in.

Never invest solely because:

- A friend recommended it

- Social media is discussing it

- It recently increased in price

Understanding should come before action.

Step 3

Start with an amount you are comfortable learning with.

Remember:

The goal is experience.

Not perfection.

Step 4

Observe your emotions.

This step is often ignored.

Pay attention to:

- Excitement

- Fear

- Anxiety

- Impatience

Investing is as much a psychological activity as a financial one.

Step 5

Review and learn.

Every investment teaches something.

The objective is continuous improvement.

What Successful Investors Understand Early

Successful investors eventually learn a powerful truth:

Investing is not about avoiding risk.

It is about taking intelligent risks.

No investment is completely risk-free.

Even keeping money idle involves inflation risk.

The objective is not to eliminate uncertainty.

The objective is to ensure that the risks you take are understood, intentional, and aligned with your goals.

A Beginner’s First-Investment Checklist

Before investing, ask yourself:

Do I understand what I am buying?

Do I know why I am buying it?

Am I comfortable if prices fluctuate?

Am I investing money I can leave untouched?

Am I making this decision independently?

If the answer is yes, you are already ahead of many beginners.

Key Takeaway

The purpose of investing is not simply to maximize returns.

It is to grow wealth while managing risk intelligently.

Every investment involves uncertainty.

Market risk, business risk, inflation risk, and behavioural risk are all part of the investing journey.

Understanding these risks before investing creates stronger decisions, greater confidence, and better long-term outcomes.

Your first investment should not be viewed as a test of your stock-picking ability.

It should be viewed as the beginning of your investing education.

Because the most successful investors are not those who never encounter risk.

They are those who learn how to manage it wisely.

In the next and final lesson, we will explore the Beginner Investor Playbook—covering the most common mistakes new investors make, the habits that separate successful investors from unsuccessful ones, and the mindset required for long-term wealth creation.

Lesson 5: The Beginner Investor Playbook

The Habits, Mistakes, and Mindset That Shape Long-Term Success

Why This Lesson Matters

By now, you understand:

- How investing works

- How to prepare your investing foundation

- How Demat accounts and brokers function

- Why risk matters

- How to make your first investment

At this point, many beginners believe they are ready.

Technically, they are.

But investing success rarely depends on technical knowledge alone.

Over time, you will discover something surprising:

Most investors do not fail because they lack information.

They fail because of behaviour.

They allow emotions to influence decisions.

They chase excitement.

They abandon plans.

They compare themselves with others.

They expect quick results from a process designed to reward patience.

This lesson focuses on the mistakes, habits, and mindset shifts that separate successful investors from unsuccessful ones.

Mistake #1: Treating Investing Like a Get-Rich-Quick Scheme

One of the fastest ways to lose money is expecting investing to make you rich quickly.

Many beginners enter the market after hearing stories about:

- Multibagger stocks

- Extraordinary returns

- Overnight success stories

What they don’t see are:

- Years of patience

- Market declines

- Mistakes

- Periods of uncertainty

Example

Imagine two investors.

Investor A expects to double money every year.

Investor B expects to build wealth steadily over decades.

Which investor is more likely to remain disciplined during difficult periods?

Usually Investor B.

Because expectations influence behaviour.

Unrealistic expectations often lead to reckless decisions.

Mistake #2: Following Tips Without Understanding

This is one of the oldest investing mistakes.

A friend recommends a stock.

A social media influencer promotes an opportunity.

A television expert shares a target price.

The investor buys without understanding the business.

The Problem

When prices rise, confidence grows.

When prices fall, panic begins.

Why?

Because conviction never existed.

Understanding creates conviction.

Tips create dependency.

A Better Rule

Never invest in something you cannot explain in simple language.

If you cannot answer:

“Why do I own this investment?”

you probably need more research.

Mistake #3: Chasing What Is Already Popular

Markets often create excitement around:

- Hot sectors

- Trending stocks

- Popular themes

This creates Fear of Missing Out (FOMO).

Example

Suppose a stock rises 80% in six months.

Everyone begins discussing it.

News channels highlight it.

Social media celebrates it.

Many investors suddenly become interested.

Not because the business improved.

Because the price increased.

This is how emotional decisions often begin.

Remember

A good investment does not become better simply because everyone is talking about it.

Popularity and quality are not the same thing.

Mistake #4: Watching Prices More Than Businesses

Many beginners check their portfolio multiple times each day.

The problem?

Most price movements have little impact on long-term value.

Example

Imagine owning part of a successful restaurant.

Would you demand a valuation update every hour?

Of course not.

You would focus on:

- Customers

- Revenue

- Profitability

- Growth

Public markets simply display prices more frequently.

That doesn’t mean they deserve constant attention.

Successful investors monitor businesses more than stock prices.

Mistake #5: Trying to Be Right All the Time

Many beginners believe successful investors never make mistakes.

The reality is very different.

Every experienced investor has:

- Bought poor investments

- Sold too early

- Missed opportunities

- Made incorrect assumptions

Mistakes are unavoidable.

The goal is not perfection.

The goal is improvement.

A Better Question

Instead of asking:

“How do I avoid every mistake?”

Ask:

“How do I ensure mistakes remain small and educational?”

That mindset creates growth.

Mistake #6: Constantly Comparing Yourself to Others

Investing is highly personal.

Different people have different:

- Goals

- Income levels

- Time horizons

- Risk tolerances

Yet many investors compare their results to others.

Example

Suppose a friend earns 40% in a year.

You earn 12%.

You may feel disappointed.

But what if:

- Your risk was lower?

- Your goals were different?

- Your strategy was more sustainable?

Comparisons often create unnecessary pressure.

The most important benchmark is progress toward your own goals.

The Habits of Successful Investors

Let’s shift from mistakes to habits.

Over time, successful investors tend to develop similar behaviours.

Habit 1: They Remain Curious

They continuously learn.

They read.

They ask questions.

They study businesses.

They improve their process.

The market rewards lifelong learners.

Habit 2: They Think Long Term

They understand that wealth creation usually takes years, not months.

Patience often becomes a competitive advantage because so many people lack it.

Habit 3: They Focus on Process

Instead of obsessing over short-term outcomes, they focus on:

- Research quality

- Risk management

- Decision-making

Good processes often produce good outcomes over time.

Habit 4: They Stay Humble

Markets have a way of humbling everyone.

Successful investors remain open-minded.

They understand that certainty is dangerous.

Humility helps them learn faster and recover from mistakes.

Habit 5: They Protect Capital

Before thinking about gains, they think about preservation.

A simple rule many experienced investors follow:

Never take a risk you do not fully understand.

Your Investor Readiness Checklist

Before moving forward, ask yourself:

Knowledge

✔ I understand how investing works.

✔ I understand risk.

✔ I understand the investments I buy.

Infrastructure

✔ My PAN and KYC are complete.

✔ My bank account is ready.

✔ My Demat account is active.

Behaviour

✔ I am not investing based on tips alone.

✔ I understand my goals.

✔ I am prepared for market fluctuations.

✔ I am thinking long term.

If you can confidently check these boxes, you are already ahead of many first-time investors.

Cherry on Top: Managing Multiple Demat Accounts

Many investors eventually open more than one Demat account.

This can happen because:

- They switch brokers.

- They test different platforms.

- They forget to close older accounts.

- They maintain separate investing and trading accounts.

Over time, tracking everything can become confusing.

A useful solution is the Central Depository Services Limited MyEasi platform, which allows investors to view holdings and monitor multiple Demat accounts through a single login and account-grouping facility when eligible.

This can help you:

- View holdings in one place

- Monitor transactions

- Access statements

- Reduce portfolio fragmentation

Many investors discover this feature only after managing multiple accounts for years.

Knowing it early can save time and confusion later.

Final Advice

If there is only one piece of advice worth remembering from this entire section, it is this:

Do Not Rush.

Most investing mistakes happen because people are in a hurry.

They rush to:

- Open accounts

- Buy stocks

- Earn returns

- Follow trends

Successful investing is rarely about speed.

It is about consistency.

You do not need to find the next multibagger.

You do not need to predict the market.

You do not need to outperform everyone else.

You simply need to:

- Keep learning

- Stay disciplined

- Avoid major mistakes

- Allow time to work in your favour

Investing is one of the few activities where patience is often rewarded more than action.

The earlier you understand that, the more powerful your investing journey can become.

Final Thought

The goal of investing is not merely to grow money.

It is to create financial freedom, flexibility, and opportunities for your future self.

Markets will rise.

Markets will fall.

Opportunities will come and go.

But investors who combine knowledge, discipline, patience, and good habits place themselves in the strongest position for long-term success.

Start small.

Learn continuously.

Think independently.

Stay invested in your education as much as your portfolio.

Both will compound over time.

Next Explore Execution Guide