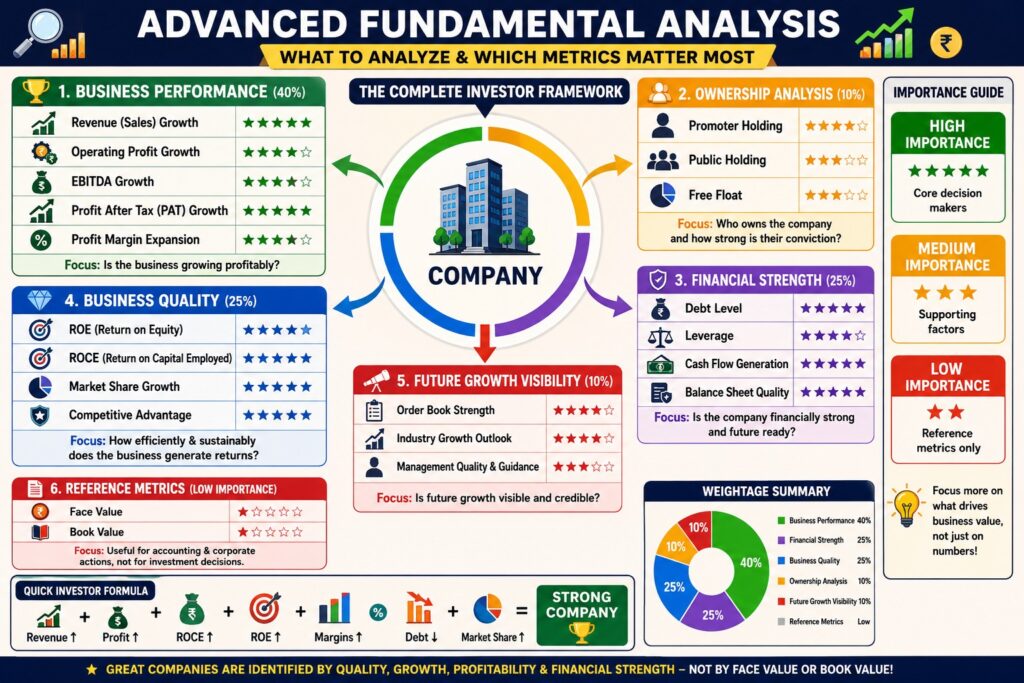

Overview

Successful investing is not about predicting tomorrow’s stock price. It is about understanding businesses well enough to identify opportunities, recognize risks, and make informed decisions.

Many investors begin by looking at stock prices, charts, or popular financial ratios. While these tools have their place, they often represent the outcome of deeper business realities. Before a company reports higher profits, gains market share, launches new products, expands capacity, or improves its competitive position, changes are usually occurring within the business itself.

Fundamental analysis is the process of studying those underlying factors.

It helps investors understand how a company makes money, how it is growing, how financially strong it is, how management allocates capital, and what factors may influence its future performance.

However, advanced fundamental analysis goes beyond simply memorizing terms such as P/E Ratio, EPS, or Book Value.

The goal is not to collect ratios.

The goal is to understand businesses. A company’s future is influenced by many factors, including revenue growth, profitability, cash flows, competitive advantages, management decisions, industry conditions, regulations, customer demand, and broader economic trends. Understanding how these factors interact often provides more insight than looking at a single financial metric.

Throughout this section, we will build a practical framework for analyzing companies. We will begin with fundamental terminology and market-cap classifications, move through financial statements and earnings analysis, learn how to interpret management commentary and concalls, explore growth drivers and growth killers, evaluate management quality, and finally understand how valuation influences investment decisions.

By the end, the objective is not simply to know more financial terms.

The objective is to develop the ability to look beyond stock prices and understand the businesses behind them.

📘 ADVANCED FUNDAMENTAL ANALYSIS

🏢 Business

(How does it make money?)

↓

📊 Financials

(P&L • Balance Sheet • Cash Flow)

↓

📈 Results

(Quarterly • Annual • Concall)

↓

🚀 Growth

(Drivers • Opportunities)

↓

👨💼 Management

(Capital Allocation • Governance)

↓

💰 Valuation

(P/E • P/B • EV/EBITDA)

↓

⚠ Risks

(Business • Financial • Industry)

↓

🎯 Investment Framework

Lesson 1: Market Capitalization & Fundamental Terminology

What You Will Learn

In this lesson, you will learn the basic language of fundamental analysis and understand how companies are classified based on their size.

By the end of this lesson, you should be able to:

✔ Understand Market Capitalization

✔ Differentiate between Large Cap, Mid Cap, Small Cap, and Micro Cap companies

✔ Understand important terms used in company analysis

✔ Learn the meaning of Revenue, Profit, EBITDA, Debt, and Order Book

✔ Understand Promoter Holding and Free Float

✔ Become comfortable with the language used by investors and analysts

Introduction

Every profession has its own language.

Before a doctor can diagnose a patient, they must understand medical terminology.

Before an engineer can design a bridge, they must understand engineering concepts.

Similarly, before analyzing companies, investors must understand the language used in fundamental analysis.

Terms such as Market Cap, Revenue, EBITDA, Debt, ROE, Promoter Holding, and Order Book appear frequently in annual reports, earnings presentations, concalls, and company discussions.

Understanding these terms is the first step toward analyzing businesses effectively.

The objective of this lesson is not to memorize definitions but to understand what these terms reveal about a company’s size, financial health, and business performance.

What Is Market Capitalization?

Market Capitalization, commonly called Market Cap, represents the total market value of a company’s outstanding shares.

It is one of the most basic ways investors classify companies.

Formula

Market Capitalization = Share Price × Number of Outstanding Shares

Example

Suppose:

Share Price = ₹500

Outstanding Shares = 10 Crore

Market Capitalization = ₹500 × 10 Crore

Market Capitalization = ₹5,000 Crore

This means the market currently values the company at ₹5,000 Crore.

Why Market Capitalization Matters

Many beginners assume that a stock trading at ₹50 is cheaper than a stock trading at ₹5,000.

This is often incorrect.

The share price alone tells us very little about the size or value of a company.

Market Capitalization provides a much better understanding of the company’s scale.

Investors should focus on the value of the business rather than the price of a single share.

Market Capitalization Categories

Companies are generally classified into four broad categories.

| Category | Approximate Market Capitalization |

|---|---|

| Large Cap | ₹20,000 Crore and above |

| Mid Cap | ₹5,000 Crore to ₹20,000 Crore |

| Small Cap | ₹500 Crore to ₹5,000 Crore |

| Micro Cap | Below ₹500 Crore |

Large Cap Companies

Large Cap companies are among the largest and most established businesses in the market.

Characteristics:

- Stable business models

- Strong market position

- Lower volatility

- Strong institutional participation

Examples often include major banks, FMCG companies, and leading IT firms.

Mid Cap Companies

Mid Cap companies have moved beyond the small-cap stage but still possess significant growth opportunities.

Characteristics:

- Balance between growth and stability

- Moderate risk

- Growing market presence

Small Cap Companies

Small Cap companies are smaller businesses with higher growth potential.

Characteristics:

- Faster growth opportunities

- Greater volatility

- Higher business risk

Micro Cap Companies

Micro Cap companies represent the smallest listed businesses.

Characteristics:

- Limited scale

- Lower liquidity

- Higher uncertainty

- Greater risk and reward potential

Face Value

Face Value is the original value assigned to a share when it is issued.

Common face values include:

- ₹1

- ₹2

- ₹5

- ₹10

Face Value is primarily used for accounting and corporate actions.

It does not indicate whether a stock is expensive or cheap.

Book Value

Book Value represents the net worth of a company based on its balance sheet.

Formula

Book Value = Total Assets – Total Liabilities

Book Value provides an estimate of what would theoretically remain for shareholders if all assets were sold and all liabilities were paid.

Promoter Holding

Promoters are the founders or controlling shareholders of a company.

Promoter Holding represents the percentage of shares owned by promoters.

Why It Matters

Promoters with significant ownership often have a stronger financial interest in the success of the business.

However, promoter holding should always be analyzed alongside other factors.

Public Holding

Public Holding refers to shares owned by investors other than promoters.

This category may include:

- Retail Investors

- Mutual Funds

- Insurance Companies

- Foreign Investors

- Other Institutions

Ownership patterns often provide insight into investor participation and confidence.

Free Float

Free Float refers to the shares available for public trading.

Not all shares of a company actively trade in the market.

Some are held by promoters or strategic investors.

Why It Matters

Lower free float often leads to higher volatility because fewer shares are available for trading.

Revenue (Sales)

Revenue, also known as Sales, represents the total value of goods or services sold by a company.

Revenue is often called the “Top Line” because it appears at the top of the Profit & Loss Statement.

Market Message

Growing revenue often indicates increasing business activity and demand.

Operating Profit

Operating Profit represents the profit generated from the company’s core business operations before interest and taxes.

It helps investors understand how efficiently the company is running its business.

Market Message

Improving operating profit often indicates stronger operational performance.

EBITDA

EBITDA stands for:

Earnings Before Interest, Taxes, Depreciation, and Amortization.

Although the term sounds complex, it is widely used to evaluate the profitability of a company’s core operations.

Market Message

EBITDA helps investors compare operating performance across businesses.

Profit After Tax (PAT)

PAT represents the final profit remaining after all expenses, interest, and taxes have been deducted.

It is commonly referred to as the Bottom Line.

Market Message

PAT reflects the actual profitability available to shareholders.

Profit Margin

Profit Margin measures how much profit remains from each rupee of revenue.

Example:

Revenue = ₹100

Profit = ₹10

Profit Margin = 10%

Market Message

Higher margins often indicate stronger business quality or pricing power.

Debt

Debt represents money borrowed by a company.

Debt can help businesses expand, build capacity, or fund growth.

However, excessive debt increases financial risk.

Market Message

Reasonable debt can support growth.

Excessive debt can become a major concern.

Leverage

Leverage refers to the use of borrowed money to increase business operations.

Leverage can amplify both profits and losses.

Market Message

Higher leverage increases both opportunity and risk.

Order Book

The Order Book represents confirmed business orders that have not yet been executed.

It is particularly important for:

- Defence Companies

- Infrastructure Companies

- Engineering Companies

- Capital Goods Businesses

Market Message

A growing order book may indicate future revenue visibility.

Market Share

Market Share represents the percentage of industry sales controlled by a company.

Example:

If the total industry size is ₹10,000 Crore and a company generates ₹2,000 Crore in sales, its market share is 20%.

Market Message

Increasing market share often indicates competitive strength and better business execution.

ROE (Return on Equity)

ROE measures how efficiently a company generates profits from shareholders’ capital.

Market Message

Higher ROE often indicates efficient utilization of shareholder funds.

ROCE (Return on Capital Employed)

ROCE measures how efficiently a company generates returns from the total capital employed in the business.

Many long-term investors consider ROCE one of the most important indicators of business quality.

Market Message

Consistently high ROCE often indicates a strong and efficient business model.

Why Terminology Alone Is Not Enough

Many beginners spend significant time memorizing financial terms.

However, successful investing requires more than definitions.

Knowing what EBITDA or ROCE means does not automatically mean an investor understands a business.

These terms are tools.

Their value comes from understanding how they connect to business performance, growth, management quality, and future prospects.

The objective is not to memorize terminology.

The objective is to understand what these terms reveal about a company.

Key Takeaway

Fundamental terminology forms the foundation of company analysis.

Market Capitalization helps classify businesses by size.

Revenue, Profit, EBITDA, Debt, and Order Book help investors understand business performance.

Promoter Holding and Free Float explain ownership structure.

ROE and ROCE provide insight into business efficiency.

These concepts create the language investors use when analyzing companies.

In the next lesson, we will move beyond terminology and learn how to read financial statements, including the Profit & Loss Statement, Balance Sheet, and Cash Flow Statement.

While this lesson introduces some of the most commonly used concepts in company analysis, many important financial ratios and valuation metrics such as P/E Ratio, P/B Ratio, EV/EBITDA, Debt-to-Equity Ratio, Current Ratio, and other analytical tools will be covered in later lessons as we build a deeper understanding of fundamental analysis.

Lesson 2: Reading Financial Statements

What You Will Learn

In this lesson, you will learn how to read the three most important financial statements used in company analysis.

By the end of this lesson, you should be able to:

✔ Understand the purpose of financial statements

✔ Read a Profit & Loss Statement

✔ Read a Balance Sheet

✔ Read a Cash Flow Statement

✔ Understand how the three statements connect with each other

✔ Identify early signs of business strength and weakness

Introduction

When investors analyze a company, they are ultimately trying to answer three simple questions:

- Is the company making money?

- Is the company financially strong?

- Is the company generating cash?

The answers to these questions are found in three financial statements:

- Profit & Loss Statement (P&L)

- Balance Sheet

- Cash Flow Statement

Together, these statements tell the financial story of a business.

Many beginners find financial statements intimidating because they contain large amounts of data and unfamiliar terminology.

However, once their purpose is understood, financial statements become much easier to read.

The goal is not to memorize every line item.

The goal is to understand what the numbers are trying to tell us.

The Three Financial Statements

Think of a company as a person.

Each financial statement answers a different question.

Profit & Loss Statement

How much money did the company make?

Balance Sheet

What does the company own and what does it owe?

Cash Flow Statement

Did actual cash enter the business?

Together they provide a complete picture of financial performance.

Profit & Loss Statement (P&L)

The Profit & Loss Statement shows the company’s financial performance during a specific period.

It tracks:

- Revenue

- Expenses

- Profitability

The P&L answers:

“Did the company make money during this period?”

Basic Structure of a P&L Statement

Revenue

↓

Operating Expenses

↓

Operating Profit

↓

Interest & Taxes

↓

Profit After Tax (PAT)

Revenue

Revenue represents the total value of goods or services sold by the company.

Revenue growth often indicates:

- Increasing demand

- Business expansion

- Market share growth

Investor Focus

Is revenue growing consistently over time?

Operating Expenses

Every business incurs expenses.

Examples include:

- Employee costs

- Raw materials

- Marketing

- Administrative expenses

Expenses should ideally grow more slowly than revenue.

Operating Profit

Operating Profit represents profit generated from the core business before interest and taxes.

Investor Focus

Is operating profit growing?

Are margins improving?

Profit After Tax (PAT)

PAT represents the final profit remaining after all expenses, interest, and taxes have been deducted.

This is the profit attributable to shareholders.

Investor Focus

Revenue growth is important.

Profit growth is even more important.

Growing revenue without growing profits may indicate underlying business challenges.

Balance Sheet

While the P&L shows performance during a period, the Balance Sheet provides a snapshot of the company’s financial position at a specific point in time.

The Balance Sheet answers:

“What does the company own and what does it owe?”

The Balance Sheet Formula

Assets = Liabilities + Shareholders’ Equity

This equation must always balance.

Assets

Assets represent resources owned by the company.

Examples:

- Cash

- Buildings

- Machinery

- Inventory

- Investments

Investor Focus

Are assets growing productively?

Liabilities

Liabilities represent obligations owed by the company.

Examples:

- Loans

- Borrowings

- Payables

- Financial obligations

Investor Focus

Is debt manageable?

Is the company becoming more dependent on borrowings?

Shareholders’ Equity

Equity represents the ownership interest of shareholders.

It can be viewed as the residual value remaining after liabilities are deducted from assets.

Investor Focus

Is shareholder value growing over time?

Why the Balance Sheet Matters

Many companies can temporarily report strong profits.

However, a weak balance sheet often creates problems later.

A strong balance sheet generally provides:

- Financial flexibility

- Lower risk

- Ability to survive difficult periods

- Capacity for future growth

Cash Flow Statement

The Cash Flow Statement tracks the actual movement of cash.

This statement answers:

“Did cash actually enter the business?”

This is important because accounting profits and cash generation are not always the same.

Why Cash Matters

Imagine a company reports:

Revenue = ₹1,000 Crore

Profit = ₹100 Crore

This appears positive.

However, if customers have not yet paid, actual cash may not have arrived.

The Cash Flow Statement helps investors verify whether reported profits are translating into real cash.

Three Sections of Cash Flow

Operating Cash Flow

Cash generated from core business operations.

Investing Cash Flow

Cash used for investments, expansion, and acquisitions.

Financing Cash Flow

Cash related to debt, dividends, and capital raising.

Operating Cash Flow

This is often the most important section for investors.

Healthy businesses generally generate positive operating cash flow over time.

Investor Focus

Is the company generating cash from its core operations?

Connecting the Three Statements

The three financial statements should not be viewed separately.

They are connected.

Example:

Strong revenue growth appears in the P&L.

New assets purchased appear in the Balance Sheet.

Cash spent on those assets appears in the Cash Flow Statement.

Together they tell a complete story.

What Investors Should Focus On

When reading financial statements, beginners often get lost in hundreds of numbers.

Instead, focus on a few important questions:

Revenue

Is the business growing?

Profit

Is profitability improving?

Debt

Is borrowing under control?

Cash Flow

Is the business generating cash?

Equity

Is shareholder value increasing?

These questions often provide more insight than memorizing every line item.

Common Mistakes Investors Make

Looking Only at Revenue

Growth without profitability may not create value.

Looking Only at Profit

Profits without cash flow can be misleading.

Ignoring Debt

Excessive debt can create significant risk.

Reading One Year in Isolation

Financial statements become more meaningful when viewed across multiple years.

Key Takeaway

Financial statements are the foundation of fundamental analysis.

The Profit & Loss Statement shows whether the company is making money.

The Balance Sheet shows financial strength and stability.

The Cash Flow Statement reveals whether profits are converting into actual cash.

Together, these statements help investors move beyond stock prices and begin understanding the financial reality of a business.

In the next lesson, we will learn how to analyze quarterly results, annual results, consolidated financial statements, management commentary, and concalls to understand how businesses evolve over time.

Lesson 3: Quarterly Results, Annual Reports & Concall Analysis

What You Will Learn

In this lesson, you will learn how investors analyze company results, annual reports, investor presentations, management commentary, and conference calls to understand the direction of a business.

By the end of this lesson, you should be able to:

✔ Understand quarterly and annual results

✔ Differentiate between standalone and consolidated results

✔ Analyze revenue, profit, margins, and cash flow trends

✔ Understand management commentary

✔ Read investor presentations effectively

✔ Understand earnings calls and concalls

✔ Evaluate future guidance

✔ Identify positive and negative business developments

Introduction

Stock prices do not move simply because a company exists.

Over time, stock prices respond to changes in business performance and future expectations.

Every quarter, listed companies report their financial results.

Investors, analysts, mutual funds, and institutions closely examine these results to understand whether the business is improving, stagnating, or deteriorating.

However, successful investors do not simply look at whether profit increased or decreased.

They try to understand:

- Why revenue changed

- Why margins expanded or contracted

- What management expects in the future

- Whether growth is sustainable

This is why result analysis is one of the most important skills in fundamental investing.

Understanding Quarterly Results

Listed companies typically publish financial results every quarter.

Quarterly results provide an update on the company’s recent business performance.

Investors use quarterly results to monitor:

- Revenue growth

- Profit growth

- Margin changes

- Debt levels

- Cash generation

- Business momentum

Quarterly results often influence short-term market reactions because they provide the latest information about business performance.

Understanding Annual Results

While quarterly results focus on short-term performance, annual results provide a broader view of the business.

Annual results help investors understand:

- Long-term growth trends

- Business consistency

- Capital allocation decisions

- Strategic direction

One strong quarter may be temporary.

Several strong years often indicate a stronger business.

Standalone vs Consolidated Results

Many companies operate through subsidiaries.

As a result, they may publish two types of financial statements.

Standalone Results

Standalone results include only the parent company.

Consolidated Results

Consolidated results include:

- Parent company

- Subsidiaries

- Joint ventures (where applicable)

Why Consolidated Results Matter

Suppose a company owns several subsidiaries.

The parent company may appear weak on a standalone basis while the overall business performs well.

For most investors, consolidated results usually provide a more complete picture of business performance.

Whenever available, investors generally focus more on consolidated numbers because they represent the performance of the entire business group.

What Investors Should Focus On First

When results are released, investors often become overwhelmed by hundreds of numbers.

Start with the most important areas.

Revenue

Is sales growth increasing?

Operating Profit

Is operational performance improving?

Profit After Tax

Is profitability growing?

Cash Flow

Is profit converting into cash?

Debt

Is leverage increasing or decreasing?

These metrics often provide a quick overview of business health.

Revenue Growth

Revenue represents the company’s sales.

Revenue growth often indicates:

- Increasing demand

- Market share gains

- Capacity expansion

- New product success

Investor Question

Is revenue growing consistently?

A single quarter may be influenced by temporary factors.

The trend matters more than one number.

Profit Growth

Revenue growth alone is not enough.

A company should ideally convert growing revenue into growing profits.

Positive Signs

- Profit growing faster than revenue

- Improving efficiency

- Better pricing power

Warning Signs

- Revenue growth but declining profits

- Rising costs

- Margin pressure

Margin Analysis

Margins reveal how much profit a company earns from its revenue.

Two companies may generate similar revenue but very different profits.

This difference often appears in margins.

Margin Expansion

Higher profitability.

Often indicates:

- Better efficiency

- Strong demand

- Pricing power

Margin Contraction

Lower profitability.

Often indicates:

- Rising costs

- Increased competition

- Weak demand

Margin trends often reveal changes before they become obvious elsewhere.

Understanding Management Commentary

Numbers explain the past.

Management commentary often discusses the future.

Management usually explains:

- Business performance

- Industry conditions

- Growth opportunities

- Risks and challenges

- Future plans

Investors should pay attention not only to what management says but also how consistently management delivers on previous promises.

Investor Presentations

Many listed companies publish investor presentations along with their results.

Investor presentations often contain information such as:

- Revenue breakdown

- Segment performance

- Market share

- Capacity expansion

- Order book

- Industry outlook

Investor presentations often provide context that financial statements alone cannot provide.

What Is a Concall?

A Concall (Conference Call) is a discussion between company management, analysts, institutional investors, and shareholders following the release of results.

During a concall:

- Management discusses performance

- Analysts ask questions

- Investors seek clarification

Concall transcripts often provide valuable insights into management thinking.

What To Look For In Concall Discussions

Experienced investors often focus on:

Growth Outlook

What is management expecting over the next few quarters or years?

Capacity Expansion

Is the company increasing production capacity?

Demand Trends

Is demand improving or weakening?

Margin Expectations

Can profitability be maintained?

Risks

What challenges does management identify?

These discussions often reveal important information before it becomes visible in financial statements.

Future Guidance & Market Expectations

One of the biggest mistakes beginners make is focusing only on historical results.

Financial statements tell us what happened.

Future guidance tells us what management expects to happen next.

Future guidance may include:

- Revenue growth expectations

- Capacity expansion plans

- Margin outlook

- Demand outlook

- New product launches

- Industry conditions

- Capital expenditure plans

Why Future Guidance Matters

The stock market is forward-looking.

Investors and institutions often care more about future growth than past performance.

A company may report strong quarterly results but issue weak future guidance.

In such situations, the stock may decline despite good results.

Similarly, a company may report average results but provide strong growth guidance, leading investors to become more optimistic about the future.

Investor Question

When reading results or concalls, always ask:

Is management becoming more optimistic or more cautious about the future?

Changes in future guidance often influence stock prices more than the reported numbers themselves.

Positive Signals Investors Look For

Examples include:

- Strong revenue growth

- Rising profits

- Margin expansion

- Growing order book

- Capacity expansion

- Debt reduction

- Positive industry outlook

- Strong future guidance

- Confident but realistic management commentary

Warning Signals Investors Watch For

Examples include:

- Revenue slowdown

- Profit decline

- Margin contraction

- Rising debt

- Weak cash flow

- Repeated guidance cuts

- Increasing competition

- Weak demand outlook

- Overly promotional management language

One warning sign may not be a problem.

Multiple warning signs deserve closer attention.

Common Mistakes Investors Make

Looking Only at Profit

Profit alone rarely tells the complete story.

Ignoring Margins

Margins often reveal business quality.

Reading Headlines Only

Result summaries rarely provide the complete picture.

Ignoring Management Commentary

Future expectations often matter as much as current results.

Ignoring Future Guidance

The market is often more interested in what may happen next than what happened last quarter.

Focusing on One Quarter

Businesses should be evaluated over multiple periods.

One quarter rarely defines a company.

Key Takeaway

Quarterly results, annual reports, investor presentations, management commentary, and concalls help investors understand how a business is evolving.

Revenue, profits, margins, debt, cash flow, and management commentary provide valuable insight into business performance.

Future guidance helps investors understand what management expects going forward and often plays an important role in determining market sentiment.

The objective is not simply to determine whether results are good or bad.

The objective is to understand why performance changed, what management expects next, and whether those expectations are realistic.

In the next lesson, we will explore Growth Drivers, Growth Killers, and the fundamental factors that can change the long-term trend of a company and its stock.

Lesson 4: Growth Drivers, Growth Killers & Trend-Changing Factors

What You Will Learn

In this lesson, you will learn how to identify the fundamental factors that influence a company’s future growth and long-term stock performance.

By the end of this lesson, you should be able to:

✔ Identify business growth drivers

✔ Recognize business growth killers

✔ Understand factors that can change a company’s long-term trend

✔ Analyze opportunities and risks more effectively

✔ Connect business developments with stock market performance

Introduction

Many investors spend significant time studying financial statements and historical results.

While understanding the past is important, investing is ultimately about the future.

The stock market constantly attempts to estimate what a company may look like several years from now.

This is why stock prices often move long before changes become visible in financial statements.

Investors are not only buying today’s business.

They are buying expectations about the future.

To understand those expectations, investors must understand the factors that drive growth and the factors that threaten it.

What Are Growth Drivers?

Growth drivers are factors that help a company increase:

- Revenue

- Profitability

- Market share

- Competitive strength

- Long-term business value

Strong businesses usually have multiple growth drivers working simultaneously.

The more sustainable the growth drivers, the stronger the long-term investment case may become.

Capacity Expansion

One of the most common growth drivers is capacity expansion.

A company cannot grow indefinitely if it lacks the ability to produce more goods or services.

Examples:

- New manufacturing plants

- Additional production lines

- New warehouses

- Expanded service capabilities

Market Message

Future revenue potential may increase.

Investor Question

Will the new capacity generate sufficient demand and profitability?

New Products & Services

Companies often create growth through innovation.

New products can:

- Increase revenue

- Expand customer reach

- Improve profitability

- Strengthen competitive positioning

Market Message

Future growth opportunities may improve.

Investor Question

Can the company successfully commercialize the new offering?

Market Share Gains

A company does not always need a growing industry to grow.

Sometimes it simply captures a larger portion of existing demand.

Example

Industry Growth = 5%

Company Growth = 15%

This may indicate increasing market share.

Market Message

Competitive strength is improving.

Industry Tailwinds

Some industries benefit from long-term structural trends.

Examples:

- Digitalization

- Defence spending

- Renewable energy

- Healthcare demand

- Financial inclusion

When industries grow, well-positioned companies often benefit.

Market Message

External conditions support growth.

Strong Order Book

The order book represents confirmed business yet to be executed.

This is especially important for:

- Infrastructure companies

- Defence companies

- Capital goods companies

- Engineering businesses

Market Message

Revenue visibility improves.

Investor Question

Can management execute efficiently?

Pricing Power

Pricing power refers to a company’s ability to increase prices without significantly reducing demand.

Companies with strong brands often possess pricing power.

Examples may include:

- Premium consumer brands

- Specialized products

- Market leaders

Market Message

Profitability may remain resilient even during inflationary periods.

Favourable Regulations

Government policies can significantly influence industries.

Examples:

- Production-linked incentives

- Defence indigenization

- Infrastructure spending

- Tax incentives

Market Message

The business environment may become more supportive.

What Are Growth Killers?

Growth killers are factors that slow, weaken, or reverse business growth.

Sometimes a company appears strong on the surface while growth killers gradually undermine performance.

Understanding these risks is equally important.

Rising Debt

Debt can support expansion.

However, excessive debt creates financial pressure.

High debt can lead to:

- Higher interest costs

- Reduced flexibility

- Increased risk during downturns

Market Message

Financial risk is increasing.

Margin Pressure

Revenue growth alone does not guarantee success.

If costs rise faster than sales, profitability may decline.

Common causes include:

- Rising raw material costs

- Wage inflation

- Competitive pricing pressure

Market Message

Business quality may be weakening.

Demand Slowdown

Every business depends on demand.

Demand may weaken due to:

- Economic slowdown

- Industry challenges

- Changing customer preferences

Market Message

Future growth may become difficult.

Increasing Competition

Competition can affect:

- Market share

- Pricing power

- Profitability

Even strong companies can struggle when competitors become more aggressive.

Market Message

Growth may become harder to sustain.

Regulatory Risks

Government regulations can create opportunities but also risks.

Examples:

- Policy changes

- Environmental restrictions

- Tax increases

- Industry-specific regulations

Market Message

Future uncertainty may increase.

Poor Capital Allocation

Strong businesses can be damaged by poor management decisions.

Examples:

- Expensive acquisitions

- Excessive debt-funded expansion

- Misallocation of capital

Market Message

Management quality becomes a concern.

Management Execution Risk

A company may announce:

- New plants

- New products

- Expansion plans

However, execution remains critical.

A good strategy poorly executed can destroy value.

Investor Question

Can management successfully deliver on its promises?

Trend-Changing Factors

Some developments have the potential to change the long-term trajectory of a company.

Examples include:

Positive Trend-Changing Factors

- Major capacity expansion

- New product success

- Significant market share gains

- Industry tailwinds

- Strong future guidance

- Large order wins

- Debt reduction

Negative Trend-Changing Factors

- Regulatory setbacks

- Debt problems

- Weak future guidance

- Market share losses

- Demand destruction

- Persistent margin pressure

These factors often influence stock prices long before they become obvious in annual reports.

Why Future Guidance Matters

One of the most overlooked growth drivers is future guidance.

Management often provides expectations regarding:

- Revenue growth

- Demand outlook

- Capacity utilization

- Margins

- Expansion plans

Markets frequently react more strongly to future guidance than current results.

Example

A company may report excellent quarterly profits.

However, if management warns about slowing demand, the stock may decline.

Similarly, average results accompanied by strong future guidance may create optimism and drive stock prices higher.

Building a Growth Framework

Whenever analyzing a company, ask:

Growth Drivers

What factors can help the company grow?

Growth Killers

What factors can slow or damage growth?

Trend-Changing Factors

What developments could significantly alter the future of the business?

The quality of investment decisions often depends on how accurately these questions are answered.

Common Mistakes Investors Make

Focusing Only on Historical Numbers

Past performance does not guarantee future growth.

Ignoring Industry Trends

Even strong companies can struggle in weak industries.

Following Growth Stories Without Evidence

Growth should be supported by business developments, not narratives.

Ignoring Risks

Every investment has both opportunities and threats.

Blindly Trusting Management Guidance

Guidance should be monitored and verified over time.

Key Takeaway

Successful investing is not just about studying the past.

It is about understanding the future.

Growth drivers help companies expand revenue, profits, and market share.

Growth killers create obstacles that can weaken performance.

Trend-changing factors often determine whether a company’s future improves or deteriorates.

Investors who learn to identify these factors gain a significant advantage because they begin analyzing businesses not only for what they are today, but for what they may become tomorrow.

In the next lesson, we will explore Management Analysis, Capital Allocation, and Corporate Governance to understand how leadership decisions influence long-term shareholder value.

Lesson 5: Management Analysis, Capital Allocation & Corporate Governance

What You Will Learn

In this lesson, you will learn how management decisions influence the long-term success of a business and how investors evaluate management quality.

By the end of this lesson, you should be able to:

✔ Understand the importance of management quality

✔ Analyze promoter holding and promoter pledge

✔ Understand capital allocation

✔ Evaluate dividends, buybacks, and debt decisions

✔ Recognize good and poor corporate governance

✔ Identify warning signs in management behavior

Introduction

Financial statements tell us what happened.

Growth drivers tell us what may happen.

Management determines whether those opportunities are successfully converted into results.

Two companies may operate in the same industry and face similar market conditions.

Yet one company may create enormous shareholder wealth while another struggles.

The difference is often management quality.

For long-term investors, understanding management is just as important as understanding financial statements.

Why Management Matters

Management makes decisions that affect:

- Growth strategy

- Capital allocation

- Debt levels

- Acquisitions

- Expansion plans

- Shareholder returns

Over time, these decisions can significantly influence the value of a business.

A strong management team can create value even in challenging environments.

A weak management team can destroy value despite favorable industry conditions.

Understanding Promoters

Promoters are typically the founders or controlling shareholders of a company.

Because promoters often own a significant portion of the business, their interests may align closely with shareholders.

Investor Question

How much of the company does management own?

This is where promoter holding becomes important.

Promoter Holding

Promoter Holding represents the percentage of shares owned by promoters.

Why Investors Monitor It

Higher promoter ownership often indicates:

- Confidence in the business

- Long-term commitment

- Alignment with shareholders

However, promoter holding alone should never be viewed as proof of management quality.

Promoter Pledge

A promoter pledge occurs when promoters use their shares as collateral for borrowing.

Why Investors Watch It Closely

High levels of pledged shares may create additional risk.

If the share price falls significantly, lenders may demand additional collateral or force the sale of pledged shares.

Market Message

Moderate pledge levels may not always be problematic.

Excessive pledging deserves closer attention.

What Is Capital Allocation?

One of the most important responsibilities of management is deciding how company capital should be used.

Every year companies generate profits and cash.

Management must decide:

- Reinvest in the business

- Acquire other companies

- Reduce debt

- Pay dividends

- Buy back shares

These decisions are known as capital allocation decisions.

Why Capital Allocation Matters

Not every rupee earned by a company creates value.

Management must allocate capital where it generates the highest long-term returns.

Good capital allocation often leads to:

- Faster growth

- Higher profitability

- Stronger balance sheets

- Greater shareholder wealth

Poor capital allocation often destroys value.

Expansion & Reinvestment

Many successful companies reinvest profits back into the business.

Examples include:

- New manufacturing facilities

- Technology upgrades

- Capacity expansion

- Product development

Investor Question

Will these investments generate attractive future returns?

Acquisitions

Companies sometimes grow by acquiring other businesses.

Acquisitions can create value when:

- Strategic fit exists

- Synergies improve profitability

- Management integrates successfully

However, expensive or poorly planned acquisitions often destroy shareholder value.

Investor Question

Is the acquisition creating value or simply increasing size?

Debt Decisions

Debt is neither good nor bad.

Its impact depends on how it is used.

Productive Debt

Debt used for profitable expansion may support growth.

Unproductive Debt

Debt used inefficiently may increase financial risk.

Investor Question

Is management using debt responsibly?

Dividends

A dividend is a portion of profits distributed to shareholders.

Some companies prefer:

- Regular dividends

- Stable payouts

Others prefer:

- Reinvesting profits for growth

Neither approach is automatically superior.

It depends on the company’s opportunities and business model.

Investor Question

Is management making rational decisions regarding cash allocation?

Share Buybacks

A buyback occurs when a company repurchases its own shares.

Buybacks can benefit shareholders when:

- Shares are reasonably valued

- Excess cash is available

- The business remains financially strong

Market Message

Management believes the company is worth investing in.

Corporate Governance

Corporate Governance refers to the systems and practices used to manage a company responsibly and transparently.

Good governance helps protect shareholder interests.

Poor governance increases risk.

Signs of Good Corporate Governance

Examples include:

- Transparent communication

- Consistent disclosures

- Responsible capital allocation

- Fair treatment of minority shareholders

- Realistic management guidance

- Ethical business practices

Warning Signs Investors Should Watch

Frequent Equity Dilution

Repeated issuance of new shares may reduce shareholder ownership.

Excessive Promoter Pledging

May indicate financial stress.

Aggressive Accounting Practices

Unusually complex reporting deserves scrutiny.

Repeated Guidance Failures

Management consistently missing its own targets may reduce credibility.

Poor Capital Allocation

Acquisitions, expansions, or investments that fail to create value.

Related Party Transactions

Transactions involving promoters or connected entities should always be reviewed carefully.

Management Commentary vs Management Actions

One of the most important lessons in investing is:

Listen to what management says.

Pay greater attention to what management does.

Promises are easy.

Execution is difficult.

Investors should compare:

- Past guidance

- Actual results

- Capital allocation decisions

- Business performance

Over time, management credibility becomes visible.

Building a Management Evaluation Framework

When analyzing management, ask:

Ownership

Do promoters have meaningful skin in the game?

Governance

Are shareholders treated fairly?

Capital Allocation

Are profits being used wisely?

Execution

Does management deliver on commitments?

Transparency

Is communication honest and consistent?

Common Mistakes Investors Make

Focusing Only on Numbers

Financial statements matter, but management determines future decisions.

Blindly Trusting Promoters

Promoter ownership alone does not guarantee quality.

Ignoring Governance Risks

Governance problems often appear before financial problems.

Chasing Narratives

Strong storytelling should never replace evidence and execution.

Key Takeaway

Management quality plays a critical role in long-term investment success.

Promoter holding, capital allocation, governance practices, debt decisions, dividends, buybacks, and execution all influence shareholder outcomes.

A strong business requires strong management to achieve its full potential.

Investors should not evaluate management based solely on promises or presentations.

They should evaluate management based on actions, decisions, and long-term results.

In the next lesson, we will explore Valuation Analysis and learn why even a great company can become a poor investment if purchased at the wrong price.

Lesson 6: Valuation Analysis & Investment Framework

What You Will Learn

In this lesson, you will learn how investors estimate whether a stock is trading at a reasonable, expensive, or attractive valuation.

By the end of this lesson, you should be able to:

✔ Understand the difference between price and value

✔ Learn commonly used valuation metrics

✔ Understand market expectations

✔ Identify overvaluation and undervaluation

✔ Understand why valuation matters

✔ Build a complete fundamental investment framework

Introduction

Many investors spend months learning how to identify good businesses.

However, identifying a good business is only half the process.

The second half is determining whether the current stock price already reflects that quality.

A great company purchased at an unrealistic valuation may generate disappointing returns.

An average company purchased at an attractive valuation may generate strong returns.

This is why valuation is one of the most important concepts in investing.

Price vs Value

One of the most important distinctions in investing is the difference between price and value.

Price

The amount currently paid for a share.

Value

What the business may actually be worth based on its future earning potential.

The market price changes every day.

The intrinsic value of a business changes much more slowly.

Successful investors try to determine whether there is a meaningful difference between the two.

Why Valuation Matters

Imagine two investors buying the same company.

Investor A purchases the company at a reasonable valuation.

Investor B purchases the company at an extremely expensive valuation.

Even if both investors own the same business, their future returns may differ significantly.

Valuation affects:

- Future return potential

- Downside risk

- Margin of safety

- Market expectations

Understanding Market Expectations

Stock prices often reflect future expectations rather than current reality.

A company growing rapidly may trade at a higher valuation because investors expect future growth.

A slower-growing company may trade at a lower valuation because expectations are lower.

Investor Question

What level of growth is already reflected in the current stock price?

This is often one of the most important questions in investing.

Price-to-Earnings Ratio (P/E)

The P/E Ratio is one of the most commonly used valuation metrics.

Formula

P/E Ratio = Share Price ÷ Earnings Per Share (EPS)

Example

Share Price = ₹500

EPS = ₹25

P/E = 20

This means investors are currently willing to pay ₹20 for every ₹1 of annual earnings.

Understanding P/E Properly

A high P/E does not automatically mean a stock is expensive.

A low P/E does not automatically mean a stock is cheap.

Valuation should always be interpreted within the context of:

- Growth

- Industry

- Business quality

- Future prospects

A fast-growing business may justify a higher valuation than a slow-growing business.

Price-to-Book Ratio (P/B)

P/B compares market value with book value.

Formula

P/B Ratio = Share Price ÷ Book Value Per Share

P/B is commonly used in:

- Banks

- Financial institutions

- Asset-heavy businesses

Investor Question

How much is the market willing to pay above the company’s net worth?

PEG Ratio

The PEG Ratio attempts to combine valuation and growth.

Formula

PEG = P/E Ratio ÷ Earnings Growth Rate

Many investors use PEG to determine whether growth justifies the current valuation.

Investor Question

Is the company’s growth supporting its valuation?

EV/EBITDA

Enterprise Value (EV) considers:

- Market Capitalization

- Debt

- Cash

EBITDA represents operating profitability.

EV/EBITDA is commonly used for comparing companies across industries.

Investor Question

What is the total cost of acquiring the business relative to its operating earnings?

Dividend Yield

Dividend Yield measures the cash return shareholders receive through dividends.

Formula

Dividend Yield = Annual Dividend ÷ Share Price × 100

Investor Question

How much cash return am I receiving relative to the current stock price?

Overvaluation vs Undervaluation

Overvaluation

A stock may become overvalued when expectations become excessively optimistic.

Characteristics may include:

- Extremely high valuations

- Unrealistic growth assumptions

- Excessive market enthusiasm

Undervaluation

A stock may become undervalued when market expectations become excessively pessimistic.

Characteristics may include:

- Low valuations

- Temporary challenges

- Strong underlying business quality

The Concept of Margin of Safety

No investor can predict the future perfectly.

This is why many investors seek a margin of safety.

A margin of safety provides protection against:

- Incorrect assumptions

- Unexpected business challenges

- Economic downturns

The greater the uncertainty, the greater the need for a margin of safety.

Valuation Is Not Timing

One of the biggest misconceptions in investing is that valuation predicts short-term price movements.

Valuation does not tell investors:

- What a stock will do tomorrow

- What a stock will do next week

Valuation helps estimate long-term attractiveness.

Markets can remain expensive or cheap for extended periods.

Why Great Companies Can Become Poor Investments

Investors often assume:

Great Company = Great Investment

This is not always true.

A great company purchased at an unrealistic valuation may deliver poor future returns.

Similarly:

Average Company = Poor Investment

This is also not always true.

Valuation matters.

Price matters.

Expectations matter.

Building a Complete Investment Framework

At this stage, you have learned:

Lesson 1

Market Capitalization & Fundamental Terminology

Lesson 2

Reading Financial Statements

Lesson 3

Results, Annual Reports & Concall Analysis

Lesson 4

Growth Drivers, Growth Killers & Trend-Changing Factors

Lesson 5

Management Analysis & Capital Allocation

Lesson 6

Valuation Analysis

Together, these lessons create a practical framework for company analysis.

A Simple Fundamental Checklist

Whenever analyzing a company, ask:

Business

How does the company make money?

Financials

Are revenue, profit, and cash flow improving?

Growth

What are the growth drivers and risks?

Management

Can management be trusted to allocate capital effectively?

Valuation

Am I paying a reasonable price?

Risk

What could go wrong?

The answers to these questions often matter more than any single ratio.

Common Mistakes Investors Make

Buying Only Because a Stock Is Falling

A falling stock is not automatically cheap.

Buying Only Because a Stock Is Rising

A rising stock is not automatically attractive.

Relying on One Ratio

No single ratio can explain an entire business.

Ignoring Future Expectations

Valuation is heavily influenced by expected future growth.

Forgetting Risk

Every investment involves uncertainty.

Key Takeaway

Valuation helps investors understand whether the current market price is reasonable relative to a company’s quality, growth prospects, and future potential.

A good business is not automatically a good investment.

The price paid for that business matters.

Successful investing requires understanding the business, evaluating management, identifying growth opportunities and risks, and determining whether the valuation provides an attractive balance between potential reward and risk.

This completes the Advanced Fundamental Analysis section and provides a framework for evaluating businesses through a long-term investor’s lens.

Conclusion

Fundamental analysis is not about memorizing ratios or predicting stock prices.

It is about understanding businesses.

Throughout this section, we explored company fundamentals, financial statements, earnings analysis, growth drivers, management quality, and valuation. Together, these concepts provide a framework for evaluating businesses more effectively.

No single metric can determine whether a company is a good investment. Successful investing requires understanding the business, identifying opportunities and risks, evaluating management, and assessing whether the current valuation is reasonable.

The goal is not to eliminate uncertainty.

The goal is to make better-informed decisions based on knowledge, logic, and disciplined analysis.

Because in the long run, successful investing is driven not by noise or predictions, but by a deeper understanding of businesses and the factors that shape their future.

Together, they form a complete analytical cycle:

Understand → Analyze → Apply

Next Explore

For Advanced Fundamental Analysis, the best external links are those that help users access company financial information directly.

Fundamental Analysis Case Studies

Below are detailed fundamental analysis case studies where financial strength, performance, and sustainability are applied to real companies.

(Case studies are added and updated regularly.)